The internet has changed shopping habits. We no longer have local retailer restrictions. Only a computer with internet connectivity is needed to buy from tens of thousands of retailers globally. No international tolls existed before 2005. Credit card processors included a currency translation fee to cover the extra costs. However, online businesses used a variety of methods to avoid the currency translation charge.

Let’s discuss Cross-Border Payments: Improving Access to Financial Services in Emerging Economies. How advancements in cross-border payment systems, blockchain, and remittance services drive financial inclusion for migrants and small businesses. How fintech solutions make international payments cheaper and more efficient.

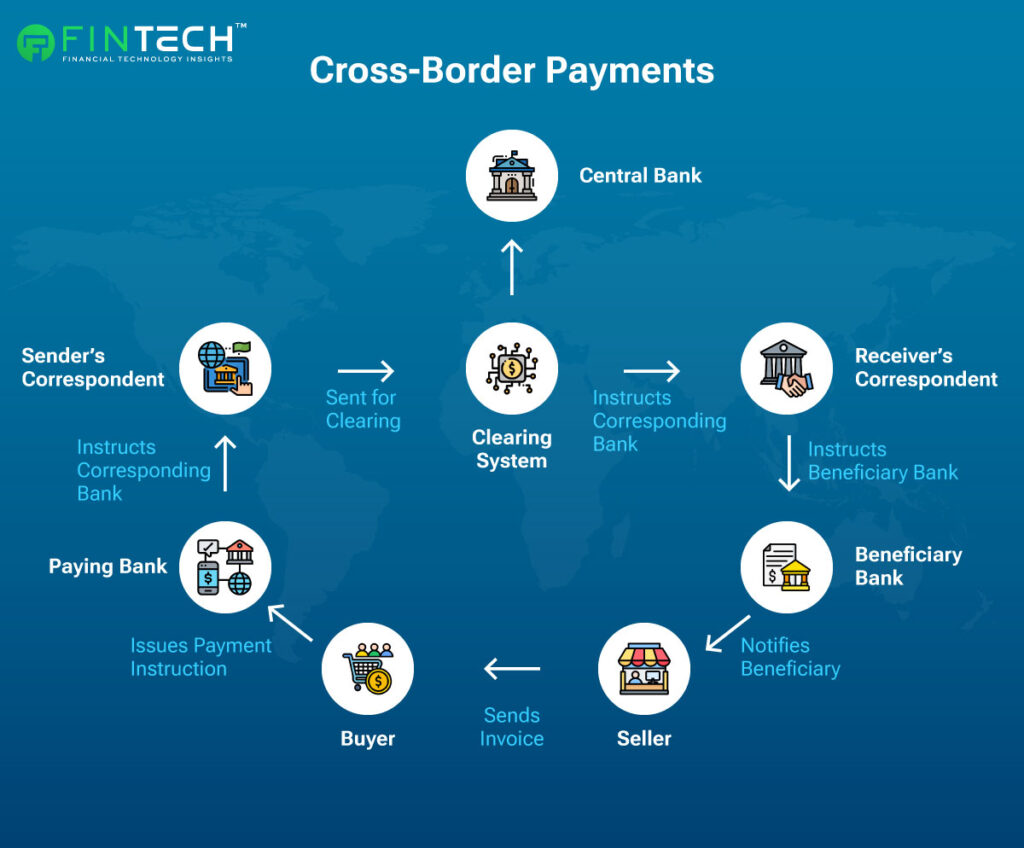

Cross-Border Payments Market: An Overview

The international commerce market has experienced an annual growth rate of 4–6% since 1995. –WTO.

The term “cross-border payments” refers to the transmission of funds between financial institutions, enterprises, or individuals in different countries. In plain terms, a transaction is classified as cross-border when the consumer and vendor (payer and payee) are located in separate countries. In the modern global economy, businesses are frequently involved in cross-border transactions, which necessitate their involvement in cross-border payments, also known as B2B cross-border payments. It is imperative that individuals who are considering cross-border business ventures have a comprehensive understanding of the concept of B2B cross-border payments. This term pertains to the transfer of funds between enterprises that are located in distinct countries. The purpose of this guide is to facilitate the administration of cross-border transactions by providing a comprehensive examination of B2B cross-border payments, including their significance, obstacles, and benefits.

Read: Top 10 Neobank Companies of the Fintech World

Cross-Border Payment Types

- International wire transfers

- Debit and credit cards

- Platforms for online payments

- Letters of Credit

- Cryptocurrencies

Players in the Cross-Border Payments Market

How Fintech Solutions Make International Payments Cheaper And More Efficient?

1. Lower Transaction Costs

- Blockchain Technology: Platforms like Ripple use decentralized ledgers to bypass intermediaries, significantly lowering transaction fees.

- P2P Transfers: Fintech apps like Wise (formerly TransferWise) use peer-to-peer matching to minimize exchange rate margins.

- Digital Wallets: Apps like PayPal and Revolut enable seamless transfers without hefty bank fees.

2. Faster Transaction Times

- Instant Settlements: Blockchain-enabled payments offer near real-time transactions by eliminating the need for manual reconciliation.

- Direct Processing: Fintech companies leverage direct integrations with local payment systems, speeding up processing times.

3. Greater Transparency

- Transparent Pricing Models: Platforms display all fees upfront, including exchange rate margins.

- Live Exchange Rates: Real-time currency rate updates provide users with clarity.

- Automated Calculations: Tools calculate the exact amount recipients will receive, removing uncertainties.

4. Improved Accessibility

- Mobile-Friendly Platforms: Apps like Payoneer and Stripe cater to freelancers and SMEs, enabling global payments via smartphones.

- API Integrations: Businesses can integrate payment solutions into their platforms for seamless transactions.

5. Advanced Security

- Encryption and Tokenization: These technologies safeguard sensitive data during transactions.

- Fraud Detection Systems: AI-powered tools monitor for suspicious activities in real time.

- Regulatory Compliance: Adherence to standards like GDPR and PSD2 ensures secure and compliant operations.

6. Innovative Business Models

- Crypto Payments: Cryptocurrencies like Bitcoin and stablecoins enable fast, low-cost international transfers.

- Multi-Currency Accounts: Fintech platforms provide accounts that hold multiple currencies, reducing the need for conversion.

- Smart Contracts: Automated agreements execute payments upon meeting predefined conditions, ensuring efficiency.

How advancements in cross-border payment systems, blockchain, and remittance services drive financial inclusion for migrants and small businesses?

- Small businesses can easily pay international suppliers and accept payments from customers across borders with minimal fees. This allows them to scale their operations, access new markets, and compete globally.

- With the use of blockchain and alternative data sources, small businesses can gain access to credit that was previously unavailable due to the lack of formal credit history or collateral. Services like Kiva and Tala offer microloans to small business owners in underserved regions, promoting entrepreneurship.

- Migrants can now open digital wallets or use apps without requiring a formal bank account. These services enable them to access basic financial services like sending money home, paying bills, and even saving without needing to go through traditional banking channels.

- Remittance services using mobile wallets, such as M-Pesa in Kenya or GCash in the Philippines, offer solutions where migrants or their families can receive and store money directly on their phones, bypassing the need for a traditional bank account.

- Financial inclusion can be more accessible and cost-effective for individuals and businesses in underserved areas if they have simpler and more affordable access to global financial transactions, which are facilitated by faster and more cost-effective cross-border payments. This has the potential to reduce the barriers to international trade and commerce, both of which can contribute to economic development.

- By reducing the time and money spent on processing and approving foreign payments, faster and more affordable cross-border payments can enhance economic efficiency. This can result in improved cash flow management, simplified business operations, and increased international investment opportunities.

- Global trade facilitation is contingent upon the provision of faster and more cost-effective cross-border payments to facilitate the payment processes between buyers and merchants in various countries. This has the potential to foster business alliances, reduce transactional risks, and expand economic growth opportunities.

- To assist their families and communities, numerous individuals send money home from their overseas employment. If transfer times and fees for international transfers are reduced and made more efficient, recipients can both save money and receive their funds more quickly.

- Developments in technology and financial infrastructure that enable instantaneous, low-cost international money transfers can stimulate financial industry innovation and competition. It is conceivable that new companies will enter the market and introduce beneficial innovations to the payment processing industry.

- Potential threats, including money laundering, fraud, and terrorist financing, may necessitate enhanced regulatory monitoring and compliance procedures as a consequence of the more rapid and cost-effective transfer of funds across borders. Financial organizations and regulatory bodies must establish a compromise between the necessity of providing adequate protection and alleviating the burden of sending payments.

- Investigating the Advantages of Cross-Border Payment: Cross-border payments are typically made between individuals, businesses, or governments in separate countries and can be made for a wide variety of reasons, including international trade, remittances, travel expenses, and investment transactions. Businesses may encounter challenges when conducting international transactions.

- Transparency and visibility are both indispensable for international money transfers. Swift gpi enables the tracking of cross-border payments in 90% of instances and their settlement within 30 minutes. Technological advancements are influencing the services we offer to our consumers. Price transparency is equally essential in the field of foreign exchange. This is brilliantly illustrated by the FedEx business model.

Conclusion

Fintech companies are consistently striving to develop innovative and customer-centric features to expedite and simplify the payment process. For example, neobanks have created new infrastructure and licenses to offer more comprehensive services without the need to go through traditional banks. Fintechs are adapting to the requirements of regulators by implementing automated compliance, algorithm-based transaction evaluations, and sophisticated Know Your Customer (KYC) systems. By capitalizing on the digital environment and state-of-the-art technologies, fintechs have outpaced traditional banks in the development of solutions for international financial transactions.

Read: Fintech Marketing: Top 10 Power Strategies to Accelerate Growth

Thanks for reading!

To share your insights with the FinTech Newsroom, please write to us at news@intentamplify.com