Be it India’s Aadhaar Program, Kenya’s M-Pesa Integration or Nigeria’s National Identification Number; we have one thing in common-Digital Identity!

Let’s discuss the Role of Digital Identity in Financial Inclusion and how blockchain, biometrics, and other technologies provide secure and scalable digital identities to unbanked populations. We will also highlight the potential of digital identity solutions in driving financial inclusion, especially in emerging markets.

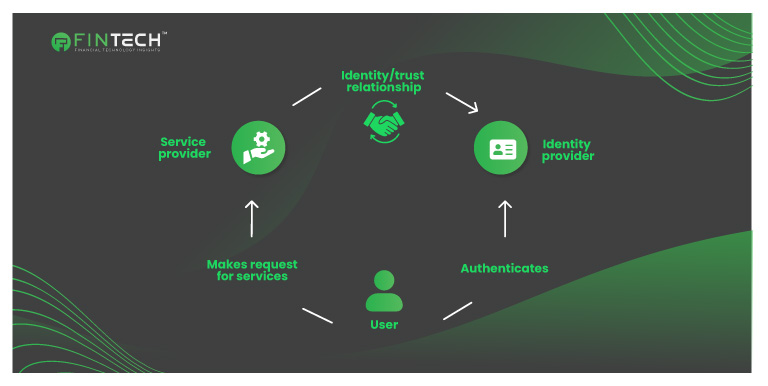

What is Digital Identity?

Digital identity is the recorded collection of measurable characteristics that a computer can use to identify an external entity in access management. The entity in question may be an individual, an organization, a software program, or an additional computer. Computer-identifiable attributes are the foundation of digital identity. For instance, a computer may be capable of recognizing an individual based on their knowledge of a password or the resonance of their voice at specific frequencies. Additionally, a computer may identify another computer by its media access control (MAC) address or IP address.

The World Bank reports that the number of account holders in India increased from 35% to 80% of the population between 2011 and 2017, largely driven by the Aadhaar biometric-based digital identity system, which enabled millions of previously unbanked individuals to access financial services. (Source: World Bank)

Despite data privacy concerns and regulatory issues, digital identity remains essential.

Jim and Sharon, two colleagues, may be capable of identifying one another by sight. However, the identity of “Jim” and “Sharon” is unknown to a computer. Instead, a computer maintains a distinct user profile for Jim and Sharon, which comprises a name, a collection of facts regarding their identity, and a set of privileges. Verifying their identity through a measurable method, such as verifying that they input the correct password, is necessary. (Jim can potentially impersonate Sharon if he knows her username and password.

It is important to note that the term “digital identity” can also refer to a computerized equivalent of government-issued personal identification documents, occasionally called “digital IDs.” However, this article concentrates on digital identity in the context of access management systems.

Fintech Insights: Top 10 CTOs Of The Fintech Industry

Common Types of Digital Identities

Individuals and organizations must be cognizant of the various digital identities they generate and employ to authorize access. This is the sole method of effectively navigating an increasingly digital landscape while preserving privacy and security.

- Device identification. Websites and cloud platforms utilize the digital identities of our smartphones and PCs to authorize or deny connections, data transfers, and access to online services. Device identities consist of unique identifiers, such as IP and MAC addresses, as well as hash codes that are calculated using factors such as the IMEI number of the device.

- Digital payment identity. As a result of the proliferation of e-commerce platforms and online payment systems such as Venmo, which allow users to purchase virtually anything, digital payment identities have become increasingly prevalent, making them more appealing to identity criminals.

- Email identification. Our email addresses frequently function as the primary user IDs in the digital realm. Individuals with personal and professional accounts will determine which to utilize depending on the system they wish to access.

- Social media profiles. The online and physical realms are connected by the identities that individuals—and frequently, bots—create on platforms like LinkedIn and Instagram. Names, profile pictures, personal and professional biographies, employment and family information, entertainment preferences, and created content are all potential components of social media identities.

- Identity of the user or account. A new digital identity is established each time an account is created on a website, cloud service, or enterprise system.

- Identity of online reputation. Business entities are especially vigilant about their online reputation identities, encompassing reviews, ratings, and comments and influencing how potential consumers perceive their products and services. If you have ever opted to forgo a restaurant due to a negative review, you have employed an online reputation identity.

How Blockchain, Biometrics, and Emerging Technologies Are Empowering Secure and Scalable Digital Identities for the Unbanked?

Using Blockchain, Biometrics, and Emerging Technologies to Empower Secure and Scalable Digital Identities for the Unbanked

The unbanked population, estimated to be over 1.4 billion globally, encounters substantial obstacles to financial inclusion due to the absence of formal identification. By providing secure, scalable, and accessible alternatives, blockchain, biometrics, and other emerging technologies are revolutionizing digital identity solutions, enabling the unbanked to engage in the global economy.

1. Blockchain: The Protection of Digital Identities

Blockchain is particularly well-suited for digital identity administration, as it is decentralized and immutable, which is particularly beneficial for the unbanked.

- Decentralized Verification: Blockchain eliminates the necessity for centralized authorities, allowing users to own and control their identities while simultaneously generating tamper-proof records.

- Interoperability: The ability of blockchain systems to integrate with various identity verification platforms guarantees scalability and global reach.

- Self-Sovereign Identity (SSI): Users can independently establish and maintain their digital identities, sharing only critical information with service providers to protect their privacy.

For instance, blockchain technology is employed by initiatives such as ID2020 to generate secure digital identities for underprivileged communities, which facilitate their access to critical services.

2. Biometrics: Improving Security and Accessibility

By utilizing distinctive physical characteristics, such as fingerprints, facial recognition, or iris scans, biometric technology is instrumental in the development of inclusive digital identities:

- Accessibility: Biometrics are especially advantageous in areas where traditional identity documentation is scarce, as they enable individuals to verify their identity with minimal requirements.

- Fraud Prevention: Using distinctive biometric markers significantly mitigates the risks of identity theft and impersonation.

- Ease of Use: Biometric authentication streamlines accessing financial services, healthcare, and government benefits.

For instance, Aadhaar, India’s biometric-based digital ID system, has facilitated millions of unbanked individuals’ access to financial and social welfare services.

3. The Bridging of the Gap: Emerging Technologies

- Artificial intelligence (AI) and machine learning: These technologies analyze data patterns in real-time to verify identities and identify fraudulent activities.

- Mobile Technology: The delivery of digital identity solutions to remote locations is facilitated by using smartphones and mobile networks.

- Cryptographic Techniques: Innovations such as zero-knowledge proofs facilitate identity verification without disclosing sensitive information.

The Role of Digital Identity Solutions in Empowering Emerging Markets

Digital identities assemble information uniquely identifying an individual, organization, application, or device online. The digital identity data of an individual may consist of their name, email address, employee ID number, social media profiles, purchase history, and identifiers for their smartphone and computer. Hardware identifiers, such as MAC addresses, unique chip identifiers, or cryptographic certificates issued by a trusted authority, are used to establish identity for a device, such as an IoT sensor. Trust is the outcome of effective digital identity administration. To function properly, online systems must be capable of establishing with certainty that an entity—whether human or otherwise—is who or what it purports to be.

- Improving Financial Inclusion: In emerging markets, the most tangible impact of robust digital identity systems is enhancing financial inclusion. Consider the Aadhaar system in India, a biometric-based digital identity initiative. With over one billion enrollments, Aadhaar has enabled millions of previously unbanked individuals to access financial services. The data is compelling; the World Bank reports that the number of account holders in India increased from 35% to 80% of the population between 2011 and 2017.

- Promoting E-Government Initiatives: Digital identity establishes the groundwork for seamless communication between governments and citizens, promoting e-governance initiatives. The transformative force of digital identity is exemplified by Estonia, a pioneer in e-governance. Estonia has become a global champion in digital governance due to the implementation of a secure digital identity system connected to various government services. This has streamlined administrative processes.

- Fueling Economic development: The symbiotic relationship between economic development and digital identity is immeasurable. For example, robust digital identity systems have been essential in Sub-Saharan Africa, where mobile money services are central to financial transactions. With its M-Pesa mobile money platform, Kenya is a prime example of a country that demonstrates how digital identity enables secure and efficient financial transactions, thereby stimulating economic development.

- Unlocking Healthcare Access: Digital identity is also transforming healthcare accessibility. Individuals may require a conventional paper record of their medical history in numerous emerging markets. The implementation of a digital identity system, as demonstrated in Rwanda, enables the construction of secure and portable health records. This enables improved healthcare delivery and empowers individuals to manage their health data.

- Enhancing Security and Mitigating Fraud: A robust mechanism for authentication and security is required due to the prevalence of digital transactions in emerging markets. When properly implemented, digital identity functions as a safeguard against deception. Nigeria’s National Identity Management Commission (NIMC) has considerably reduced identity-related fraud and provided legal identity to citizens through its digital identity initiative.

Digital identity solutions hold transformative potential for emerging markets. These systems can empower millions by enabling financial inclusion, improving access to essential services, and driving economic development. However, achieving this vision requires addressing existing challenges through strategic collaboration and innovation. As emerging markets embrace the digital age, robust identity systems will serve as a cornerstone of inclusive growth and resilience.

Conclusion

The unbanked are now able to access financial services and participate in the global economy as a result of the transformation of digital identity management by blockchain, biometrics, and emergent technologies. These innovations establish the groundwork for a financial ecosystem that is more inclusive and equitable by overcoming obstacles to identity verification.

Read: Impact of Fintech on Retail Banking Trends

Read: Top 10 FinTech Cybersecurity Challenges in 2025

Read: Fintech Marketing: Top 10 Power Strategies to Accelerate Growth

We will be back with more exciting articles in the fintech domain!

Write to us for any suggestions.