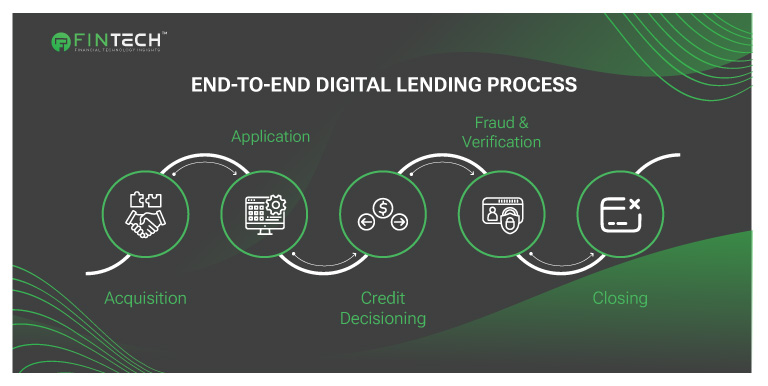

What is Digital Lending?

The digitization of the lending process offers banks a variety of significant advantages, such as enhanced customer experience, improved decisions, and substantial cost savings. Additionally, it is an undertaking that is both intricate and difficult.

Digital lending is the practice of offering loans online rather than through traditional, in-person methods. Websites and mobile apps allow borrowers to apply, get accepted, and receive loans. Lenders deposit funds into borrowers’ bank accounts, and borrowers repay online. This electronic alternative speeds up lending, eliminates paperwork, and makes it more accessible.

Digital lenders offer personal, business, payday, and mortgage loans.

Read latest fintech articles: Fintech for Women’s Financial Empowerment

What is Risk-Based Pricing?

Credit risk-based pricing offers consumers variable interest rates and loan terms based on their creditworthiness. Risk-based pricing considers a borrower’s credit score, unfavorable credit history (if any), employment status, income, debt level, assets, collateral, co-signer, and other factors that affect their capacity to repay the loan. It does not evaluate race, color, national origin, religion, gender, marital status, or age, which the Equal Credit Opportunity Act prohibits. Lenders tailor risk-based pricing analysis to borrower credit scores, debt-to-income, and other loan approval factors. Industry lenders’ risk tolerances and loan risk management procedures vary. These strategies can set borrower risks and parameters.

Risk-based pricing bases loan terms on credit profile. Risk-based pricing and underwriting examine a borrower’s loan application for these traits. Lenders usually base risk-based analysis on credit score and debt-to-income. However, lenders also carefully review a borrower’s credit report, including delinquencies and serious bad factors like bankruptcy.A 2011 federal risk-based pricing rule requires lenders to notify borrowers of certain risk-based pricing scenarios.

Read latest fintech articles: The Rise of Neo-Banks: Transforming Financial Access in Emerging Markets

Why is Fraud Prevention Important in Digital Lending?

1. AI/ML Implementation

These tools may identify fraud trends in data sets. ML and AI algorithms can uncover unexpected patterns in large data sets that may indicate fraud. These technologies may constantly learn and improve as they work. AI can detect unusual transaction patterns, assess loan applications’ risk, and flag suspicious activity for further review. Learning from new data allows AI-powered systems to adapt to fraud schemes and improve detection rates.

2. Device Fingerprinting and Biometric Authentication for Fraud Monitoring

Fingerprint scanning and other identity verification procedures may reduce identity theft and unethical account access. Systems continuously monitoring lending activity can detect suspect trends or behaviors and prevent loan fraud. Blockchain is decentralized. It can boost loan security and transparency. Fraudsters find it harder to alter loan records.

3. Understanding Regulatory Guidelines to Read Fine Print

- Interest rates

- Any additional fees

- The loan repayment method

4. Communicate openly. Lenders should be transparent in their actions. You must receive precise information about:

- Loan amount Interest rates

- Total costs

- Repayment plans

Sharing this data builds trust and helps you choose a loan. Remember, trustworthy lenders prioritize client protection to build confidence. Online lenders must safeguard personal and financial data. Customer support can improve the entire experience if it is smooth.

5. Practice ethical lending

Ethics in lending builds and maintains consumer confidence. Lenders should avoid predatory loan practices like high interest rates and hidden fees. Responsible lending builds trust and distinguishes real from phony lenders.

You must choose a responsible lender who prioritizes your finances. You may build a good relationship with an honest lender this way.

6. Accountable Customer Support

Customer support must be reliable and accessible to retain trust and detect loan fraud. There are several ways to communicate, such as by phone or email. Online chat and social media are more ways to reach customer service. Support staff are competent and quick to resolve concerns. It can detect fraud early. A sound support system shows lenders care and builds trust with loan applicants.

7. Reporting Strange Behavior

Online lending honesty hinges on borrowers understanding the importance of reporting fraud. This contains clear instructions for notifying local police or cybersecurity departments.You must report suspicious activity. Early reporting helps authorities spot and stop fraud. Thus, they can prevent future victims from falling into the same traps.

8. Understanding Loan Terms

Borrowers must thoroughly study and comprehend their loan terms. This prevents fraud and ensures equitable lending. People must comprehend everything about APR .You must also understand the loan payback plan and associated expenses. Loan applicants who know about hidden fees. If you learn finances and read carefully, you can make smarter decisions and avoid unjust financing.

9. Communicate clearly with the lender

Clear communication builds online lending trust. This includes delivering simple loan products and step information to borrowers without jargon. Lenders must reveal all costs, including interest rates and repayment options. Open and honest communication strengthens relationships. Transparency and customer service can help online lenders build trust. Their brand is difficult to copy for fraudsters.

Read latest fintech articles:The Role of Open Banking in Driving Financial Inclusion

Real-World Impact: Statistics and Insights

- Lending Fraud Losses In 2022, U.S. consumers reported over $8.8 billion in losses due to fraud, a 30% increase from the previous year (Source: Federal Trade Commission). Experian reported a 41% increase in fraud attempts among digital lenders following the pandemic.

- Implementation of Fraud Prevention Instruments- According to a survey conducted by Deloitte, 83% of fintech lenders have implemented AI-based fraud detection systems. For companies such as Onfido and Jumio, identity verification technologies have reduced loan fraud by as much as 40%.

- Efficiency of Risk-Based Pricing- According to a McKinsey study, lenders have decreased default rates by 25% due to risk-based pricing.

Read latest fintech articles: The Future of Digital Wallets and Payment Systems for the Unbanked

Leading the Way: Major Brands

- Newcomer: Upstart’s platform employs artificial intelligence (AI) and machine learning to evaluate borrower risk and prevent fraud by analyzing more than 1,000 variables.

- Zest AI: Renowned for its sophisticated credit underwriting solutions, Zest AI incorporates fraud detection into its risk models to enhance the accuracy of lenders’ decisions.

- Onfido: Their tools guarantee secure onboarding for digital lending platforms, with a focus on identity verification.

- Plaid assists lenders in verifying borrower information and mitigating fraud risks by offering secure financial data connections.

Read latest fintech articles: Sustainable Finance and Financial Inclusion: The Growing Intersection

Conclusion

Fraud risk should be considered in your risk-based pricing strategy. How can you incorporate it into your underwriting?

Your fraud department might possess the necessary information. You can integrate fraud risk into your pricing strategy by utilizing a fraud detection and prevention platform equipped with third-party data analytics, orchestration, and machine learning. One integrated with reliable third-party data intelligence providers can be deployed out of the box with built-in or custom rules that may be added, deleted, or altered to fit your institution’s risk profile and tolerances. No IT or programming skills are needed to drag and drop adjustments. Its external and internal data inputs and built-in machine learning improve its ability to accurately profile fraud and compliance risk, allowing the preferred platform to generate metrics and flags for risk-based pricing strategies.

Read latest fintech articles: Cross-Border Payments: Improving Access to Financial Services in Emerging Economies

Read: Fintech in Hospitality: Top 10 Fintech Solutions for Hotels

To participate in our interviews, please write to us at news@intentamplify.com