Introduction

Central Bank Digital Currencies (CBDCs) are transforming the financial services domain, which connects traditional fiat systems with the latest digital technology. The necessity for financial systems that are efficient, secure, and inclusive has increased as global economies continue to develop, which has facilitated the adoption of CBDCs. Central banks issue and regulate these digital currencies, which have become an essential instrument for modernizing monetary systems, the promotion of financial inclusion, and the resolution of the obstacles presented by cryptocurrencies and other decentralized digital assets.

The concept of CBDCs has acquired momentum on a global scale, with several countries investigating its potential through pilot programs and policy frameworks. Advanced initiatives are being spearheaded by nations such as the Bahamas, Sweden, and China, while the United States and the European Union thoroughly examine the implications of incorporating CBDCs into their financial ecosystems. The increasing interest in CBDCs is attributable to their capacity to facilitate quicker transactions, reduce cross-border payment costs, and offer a stable, government-backed alternative to volatile cryptocurrencies.

Nevertheless, implementing CBDCs is not without its intricacies. Policymakers, economists, and technologists are discussing privacy, cybersecurity, and potential disruptions to conventional banking systems. These challenges underscore the significance of a meticulously calibrated strategy to guarantee that implementing CBDCs enhances financial stability and consumer trust rather than undermines it.

It also investigates the primary issues and challenges associated with their adoption and the significant developments and future trends influencing their trajectory. This article offers a comprehensive comprehension of the emerging global financial framework’s role for CBDCs, from their potential to revolutionize financial inclusion to the technological innovations that underpin their functionality.

CBDCs can potentially revolutionize how governments, businesses, and individuals interact with money as the world approaches a predominantly digital economy. By the conclusion of this guide, readers will acquire valuable insights into the opportunities and challenges presented by this innovative development in modern finance.

Read: Fintech in Hospitality: Top 10 Fintech Solutions for Hotels

TOC

- What is a Central Bank Digital Currency (CBDC)?

- Uses of CBDCs

- CBDCs of Different Types

- Issues Concerning CBDCs

- Problems Caused by CBDCs

- Top 5 Key Developments In CBDC

- A Look into 2025 Trends for CBDC

- FAQ’s

- Conclusion

What is a Central Bank Digital Currency (CBDC)?

The term “central bank digital currency” (CBDC) refers to a specific kind of digital money that the central bank of a country issues. It resembles cryptocurrencies, except the central bank establishes its value, making it equivalent to the country’s fiat currency. Numerous countries are developing CBDCs, and some have even implemented them. It is crucial to comprehend the nature of CBDCs and their implications for society, as numerous nations are currently investigating methods to transition to digital currencies.

A CBDC is issued by a nation’s monetary authority, or central bank, to facilitate the implementation of monetary and fiscal policies and to promote financial inclusion Numerous nations are investigating the potential impact of CBDCs on their financial networks, economies, and stability. Individuals and nations must comprehend central bank digital currencies, as certain economies worldwide are transitioning to their utilization.

The government issues fiat money, which lacks the physical backing of gold or silver. It is regarded as a legal tender that can be exchanged for products and services. In the past, fiat money was represented by banknotes and coins. However, technological advancements have enabled governments and financial institutions to augment physical fiat money with a credit-based currency model that digitally documents transactions and balances. The physical currency continues to be extensively accepted and exchanged.

Nevertheless, its utilization has declined in certain developed nations, and the pandemic has further exacerbated this trend. Additionally, introducing and developing blockchain technology and cryptocurrency have sparked a renewed interest in digital currencies and cashless societies. The government and central banks are currently investigating the utilization of government-backed digital currencies. Like fiat money, the issuing government would fully support these currencies upon implementation.

Read: Top 10 Neobank Companies of the Fintech World

Uses of CBDCs

Many individuals lack access to financial services in the United States and numerous other countries. In 2023, 6% of adults in the United States had no bank account. Two The figures are significantly higher in numerous other countries.

When this is taken into consideration, the fundamental goals of CBDCs are as follows: CBDCs want to give organizations and customers who engage in financial transactions with a number of benefits, the most important of which are financial security, convenience, transferability, privacy, and accessibility. The expenses of maintaining a complicated financial system should be reduced, the prices of conducting transactions across international borders should be reduced, and individuals who use other ways of money transmission should be provided with options that are less expensive.

Diminish the hazards associated with using digital currencies, or cryptocurrencies, in their present state. The value of cryptocurrencies is subject to significant fluctuations, rendering them highly volatile. This volatility has the potential to impact the stability of an economy significantly and result in severe financial duress for numerous households. Households, consumers, and businesses would have a secure method of exchanging digital currency through CBDCs, which are guaranteed by the government and regulated by a central bank. Using a CBDC, a central bank can also implement monetary policies to control growth, influence inflation, and ensure stability.

Read :Top 5 Reasons Why Sysdig Is Used by Goldman Sachs

CBDCs of Different Types

CBDCs are classified into two categories: wholesale and retail. Financial institutions primarily utilize wholesale CBDs, while consumers and businesses utilize retail CBDs. Four

Wholesale CBDCs

Wholesale CBDCs operate similarly to central bank reserves. The central bank grants an institution an account to deposit funds or resolve interbank transfers. Central banks may establish interest rates and regulate lending by employing monetary policy instruments, including reserve requirements or interest on reserve balances.

Retail CBDCs

They eliminate the intermediary risk, the possibility that private digital currency issuers may go insolvent and lose customers’ assets.

- They differ in how individual users access and utilize their currency.

- Access to token-based retail CBDCs requires private, public, or both keys. This validation procedure allows users to execute transactions anonymously.

- Digital authentication is necessary to access an account in account-based retail CBDCs.

- We can develop and implement the two varieties of CBDCs so that they operate within the same economy.

Issues Concerning CBDCs

The Federal Reserve has identified issues CBDCs addresses and matters that must be addressed before a CBDC can be designed and implemented.

Issues Addressed By CBDCs

- Free from credit and liquidity risk

- Lower cross-border payment costs

- Support the international role of the dollar

- Aim for financial inclusion

- Expand access to the general public

Issues Created by CBDCs

- Financial structure changes

- Financial system stability

- Monetary policy influence

- Privacy and protection

- Cybersecurity

Problems Addressed by CBDCs

- Reduce the risk of third-party events, such as bank failures or raids.

- Increased jurisdictional cooperation between governments and the reduction of complex distribution systems can reduce high cross-border transaction costs.

- Implementing a financial structure within a country eliminates the cost and provides financial access to the unbanked population.

- This technology can eliminate costly infrastructure by directly connecting consumers and central institutions.

Read: 10 AI ML Applications in the Identification and Prevention of Different Types of Fraud

Problems Caused by CBDCs

- The potential impact of a significant change in the United States’s financial structure on the economy, household expenses, investments, banking reserves, interest rates, and the financial services sector is undetermined.

- A transition to CBDC, the impact of which is currently unknown, may impact the stability of a financial system. For instance, insufficient central bank liquidity may prevent withdrawals during a financial crisis.

- Central banks implement monetary policy to influence inflation, interest rates, lending, and spending, which impact employment rates. Central banks must possess the necessary instruments to influence the economy positively.

- One of the most significant factors driving cryptocurrency is privacy. Authorities’ monitoring of financial offenses is crucial for CBDCs, as it supports efforts to combat money laundering and the financing of terrorism. Therefore, an appropriate level of intrusion is necessary.

- Hackers and criminals have targeted cryptocurrency. A central bank’s digital currency would likely attract the same criminals. Consequently, a robust strategy to prevent system penetration and the seizure of information and assets would be necessary.

Top 5 Key Developments In CBDC

- BDF and HKMA Unlock New CBDC Cross-Border Opportunities

- Reltime Enables Merchants to Accept Payments in Digital Currencies and CBDCs Globally

- Bundesbank and MIT Media Lab to Conduct Joint Research Into CBDC

- Swift Sets Industry Up for Seamless Introduction of CBDCs for Cross-Border Transactions as Interlinking Solution Finds More Use Cases

- Mastercard Demonstrates How Existing Commercial Bank Rails Could Drive Adoption of Central Bank Digital Currencies (CBDCs) in the Future

A Look into 2025 Trends for CBDC

1. More Countries Launching CBDCs

In 2025, more countries are expected to roll out their CBDCs. According to recent reports, several nations, including China, India, and Sweden, are in advanced stages of CBDC development. The success of China’s digital yuan pilot has inspired other central banks to accelerate their projects.

For instance:

- China: The digital yuan, or e-CNY, is being integrated into everyday payment systems, from shopping to public transportation.

- Europe: The European Central Bank (ECB) is actively exploring the digital euro, aiming to make it a practical alternative for cash and card payments.

2. Focus on Financial Inclusion

CBDCs could provide a simple and accessible way for people to participate in the economy using just a smartphone.

For example:

- In Africa, CBDCs could help bring financial services to remote areas where traditional banking infrastructure is scarce.

- Governments can use CBDCs to distribute social welfare payments directly to citizens, reducing delays and corruption.

3. Private Sector Collaboration

Central banks will likely partner with fintech companies, payment service providers, and technology firms to develop user-friendly platforms and apps for CBDCs.

Collaborations may include:

- Fintech Innovations: Companies like PayPal and Visa could integrate CBDCs into their existing platforms, making it easier for consumers to adopt.

- Retail Partnerships: Stores and e-commerce platforms might offer discounts or incentives for CBDC transactions to encourage usage.

4. Enhanced Cross-Border Payments

Cross-border transactions are often slow and expensive, but CBDCs could change that. Central banks are exploring ways to link their digital currencies for seamless international payments.

Key initiatives include:

- BIS Innovation Hub: The Bank for International Settlements is working on projects to connect multiple CBDCs across borders.

- Pilot Programs: Countries like Singapore and Thailand have successfully tested cross-border CBDC payments, showing the potential for real-time international transactions.

5. Regulatory Frameworks and Security

As CBDCs evolve, regulatory frameworks will become more robust to ensure security, privacy, and compliance. Governments are working on laws and guidelines to prevent misuse, such as money laundering or cyberattacks.

Security measures may include:

- Strong encryption and fraud detection systems.

- Transparent governance to build public trust.

6. Integration with Emerging Technologies

CBDCs are likely to leverage emerging technologies like blockchain, artificial intelligence (AI), and the Internet of Things (IoT). These technologies can enhance efficiency and offer innovative use cases.

Smart Contracts: CBDCs could be programmed to execute automatic payments based on predefined conditions.

7. Environmental Considerations

With growing concerns about climate change, central banks are prioritizing the environmental impact of CBDCs. Unlike energy-intensive cryptocurrencies, CBDCs can be designed to operate efficiently and sustainably.

Efforts may involve:

- Using eco-friendly technologies for CBDC infrastructure.

- Supporting green initiatives by incorporating carbon footprint tracking in CBDC systems.

FAQ’s

How does CBDC differ from cryptocurrency?

CBDCs and cryptocurrencies are both digital, but they differ significantly. CBDCs are issued and regulated by central banks, making them a stable and legal tender backed by a government. Cryptocurrencies, like Bitcoin and Ethereum, operate on decentralized networks without government oversight, often experiencing high volatility. Additionally, CBDCs are designed for broad adoption within existing financial systems, ensuring trust and security, while cryptocurrencies are often used for speculative investments or niche applications. Unlike CBDCs, most cryptocurrencies are not linked to any real-world asset or institution.

Why are countries developing CBDCs?

Countries are developing CBDCs to modernize their financial systems, enhance payment efficiency, and increase financial inclusion. CBDCs enable governments to reduce reliance on cash, lower transaction costs, and combat financial crimes by improving transparency. They also offer a response to the growing popularity of cryptocurrencies and stablecoins, ensuring that central banks retain control over monetary policy. By introducing CBDCs, nations aim to support innovation while safeguarding financial stability and trust in their currencies.

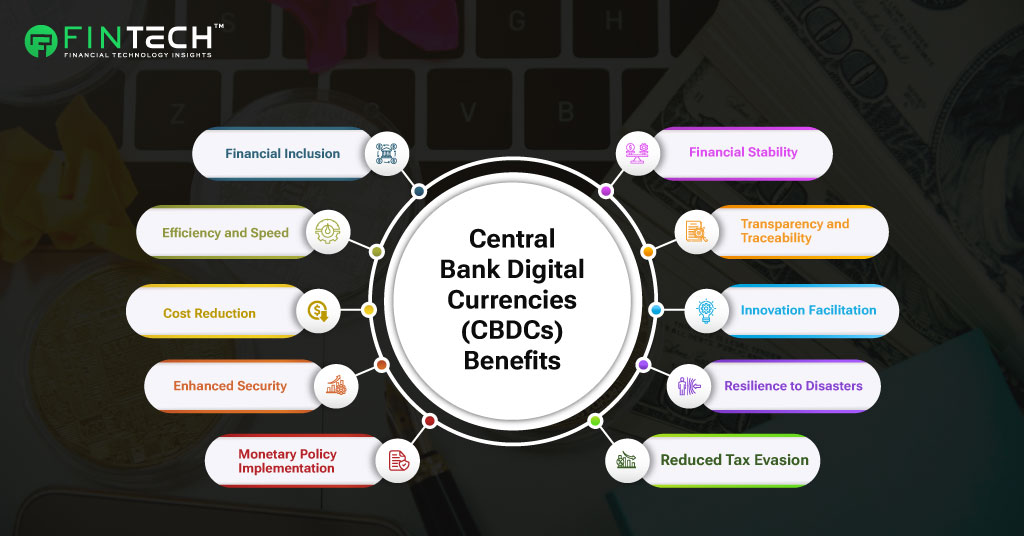

What are the key benefits of CBDCs?

CBDCs offer several benefits, including faster and cheaper transactions, improved financial inclusion, and reduced reliance on physical cash. They enhance payment system resilience by providing an alternative to private payment platforms and mitigate risks associated with currency counterfeiting. CBDCs also enable better monitoring of financial flows, aiding in combating money laundering and tax evasion. Furthermore, they ensure central banks maintain control over monetary policy in an increasingly digital economy.

How do CBDCs enhance financial inclusion?

CBDCs can promote financial inclusion by providing digital payment options to unbanked or underbanked populations. Accessible through smartphones or basic digital wallets, CBDCs eliminate barriers posed by traditional banking systems, such as account fees or geographical limitations. They enable individuals to participate in the digital economy, fostering economic growth and inclusion. Additionally, CBDCs can facilitate government-to-person payments like subsidies and pensions, ensuring funds reach recipients directly and securely.

Are CBDCs secure?

Yes, CBDCs are designed with robust security features to prevent fraud and cyber threats. Central banks leverage advanced encryption technologies and blockchain or distributed ledger systems to ensure data integrity and transaction safety. Unlike cryptocurrencies, which can be prone to hacking and volatility, CBDCs operate within a regulated framework, ensuring transparency and trust. Central banks continually assess and update security protocols to adapt to emerging threats in the digital landscape.

How do CBDCs impact traditional banking?

CBDCs could significantly impact traditional banking by reducing the reliance on commercial bank deposits for payments. If individuals choose to hold CBDCs directly with central banks, it might reduce liquidity for commercial banks, affecting their ability to lend. However, central banks can design CBDCs to complement existing banking systems, ensuring they do not destabilize the financial ecosystem. Collaboration between central banks and commercial banks is key to ensuring seamless integration.

Will CBDCs replace cash?

Not really! They are intended to complement physical currency, offering a digital transaction alternative. Many people still rely on cash for various reasons, including lack of digital access or personal preference. Central banks aim to provide a balanced approach, ensuring inclusivity while promoting the adoption of CBDCs. Over time, as digital infrastructure improves, the use of cash might decrease naturally.

How are CBDCs being tested globally?

The feasibility of CBDCs is being investigated by a number of nations through the implementation of pilot programs. For instance, China’s digital yuan has been subjected to intensive testing in retail situations as well as international financial operations. While the Federal Reserve of the United States is looking into potential applications of a digital euro, the European Central Bank is looking into what a digital euro may be. The technological, legislative, and sociological ramifications of CBDCs are being evaluated through these pilot projects. These global projects, such as Project Dunbar by the BIS, aim to investigate the utilization of CBDC across international borders, stressing the importance of international collaboration in this area.

Conclusion

Digital currencies issued by central banks, also known as CBDCs, are helping to pave the way for the future of money. By combining the ease of use of digital technology with the reliability of central banks, central bank digital currencies (CBDCs) have the potential to alter how economies operate and how we handle financial transactions. They claim to make payments more quickly, to increase financial inclusion, and to provide an alternative to cryptocurrencies that is backed by the government.

However, the road to fully adopting CBDCs isn’t without its challenges. Concerns around privacy and security and how they might disrupt traditional banking systems need thoughtful solutions. For CBDCs to succeed, policymakers must carefully balance innovation with stability and ensure that these digital currencies work for everyone, from governments to businesses to everyday people.

As countries continue experimenting and refining their CBDC strategies, we enter an exciting new era for money. How we earn, save, and spend might look very different shortly, but with the right approach, these changes could lead to a more inclusive and efficient global financial system.

Thank you for exploring this journey with us! If you’d like to share your thoughts or join the discussion, please contact us at news@intentamplify.com.

Read: Fintech Marketing: Top 10 Power Strategies to Accelerate Growth

Thanks for reading!