Let’s talk about the regulatory developments in financial inclusion, such as global trends and local challenges. We shall also highlight the analysis of new regulations and policies that foster or hinder financial inclusion across different geographies and how the CFOs can prepare for regulatory changes and ensure compliance while driving financial inclusion initiatives.

What is Financial Inclusion?

Financial inclusion is the provision of financial products and services that are both affordable and beneficial to individuals and businesses, such as transactions, payments, savings, credit, and insurance. These products and services are provided sustainably and responsibly. Financial inclusion is a strategy that endeavors to expand the availability of commonly used financial services to a broader segment of the global population at a reasonable cost.

According to the Global Findex database, approximately 1.7 billion adults worldwide remain unbanked, meaning they do not engage in any basic financial services. This highlights the significant barriers to financial inclusion that need to be addressed for broader global economic participation. Source

Other marginalized groups, geographical regions, consumers of a specific gender, consumers of a specific age, or financial inclusion may be the subject of discussion. Financial inclusion may lead to an increase in economic growth, consumer awareness, and innovation. Advancements in fintech, such as digital transactions, are making financial inclusion more feasible. The financial sector consistently develops innovative strategies to provide products and services to the global population, frequently generating profits. This achievement is commendable. For instance, the increasing usage of financial technology (or fintech) has facilitated the creation of innovative solutions to the problem of financial service inaccessibility. It has introduced new methods for individuals and organizations to obtain services at reasonable prices.

Fintech Insights: Top 10 Strategies for Effective Fintech Branding

The future of financial inclusion is anticipated to be considerably impacted by advancements in fintech, such as artificial intelligence, blockchain, and digital currencies. Additionally, regulatory developments and a greater emphasis on data privacy and security will influence financial inclusion initiatives worldwide.

Financial inclusion is associated with various hazards, including potential exploitation by unscrupulous lenders, data privacy concerns with digital financial services, and over-indebtedness. The act of ensuring that all individuals, particularly those who are marginalized and underserved, have access to financial services that are both affordable and appropriate is known as financial inclusion. It is intended to equip individuals with the requisite resources, such as savings accounts, credit, insurance, and digital payment options, to facilitate the management of their finances, participation in the formal financial system, and development of economic resilience.

Financial inclusion facilitates economic growth by encouraging entrepreneurship, increasing savings, and expanding investment opportunities. It leads to an increase in productivity and job creation by promoting consumer expenditure and business growth. Additionally, a financially inclusive economy is more likely to attract foreign investment and contribute to realizing sustainable development objectives.

Read: Top 5 Strategies for Cloud Security Regulations in Financial Services by Sysdig

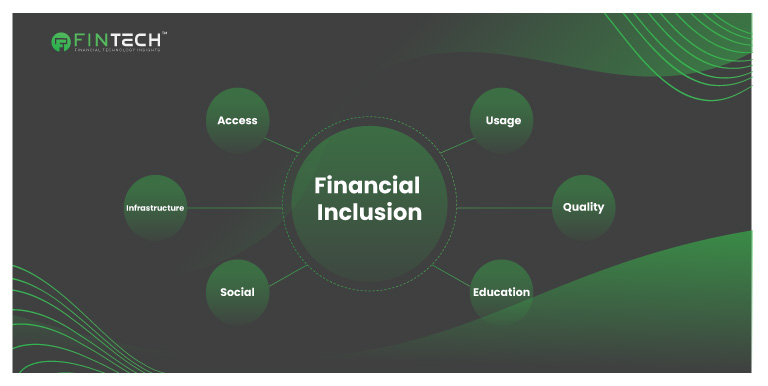

The Four Dimensions Of Financial Inclusivity

The financial inclusion framework allows leaders to evaluate and resolve their organization’s financial inclusion strategy in four distinct areas: the broader ecosystem, community, offerings, and organization. Firms should assess the strategic, operational, and technological influence on the stakeholders of an organization, including its personnel, customers, vendors, partners, and the external marketplace, within each of the four dimensions. Leaders can use this exercise to establish new market relationships, develop strategies, and designate priorities to transition from strategy to action. Financial institutions should comprehensively address the issues within the context of an organization’s financial inclusion strategy to identify a distinctive competitive advantage. When leaders address and align the four dimensions within their financial inclusion objectives, they can achieve the highest potential benefits of financial inclusion.

Financial Inclusion : Global Trends

- Poverty and inequality are diminished by financial inclusion. Financial inclusion allows marginalized and low-income individuals to access formal financial services, including deposits, credit, and insurance. Financial inclusion can assist in alleviating poverty and reducing economic disparities by providing individuals with the resources necessary to manage their finances and engage in income-generating activities.

- Economic expansion is stimulated by financial inclusion. A general argument is that the economy is more likely to be engaged by more individuals with access to financial services. Economic growth and stability are promoted in both local communities and national economies due to increased financial inclusion, which results in increased savings, investment, and entrepreneurship.

- Small enterprises are encouraged by financial inclusion. Traditional banking sources frequently present obstacles to small enterprises’ pursuit of credit. Innovative lending models and online platforms can provide entrepreneurs the necessary funding to expand their enterprises, promoting financial inclusion.

- Demographics that are otherwise marginalized are empowered by financial inclusion. For instance, financial inclusion initiatives designed to empower women can foster economic empowerment and gender equality. Women can achieve enhanced educational opportunities, improved health outcomes, and increased decision-making authority within households by gaining more control over their finances by providing access to financial services.

- Innovation is fostered by financial inclusion. The financial sector is stimulated by financial inclusion, which results in the creation of new technologies and fintech solutions tailored to underserved populations’ requirements. These innovations can potentially enhance the financial services industry and benefit the broader financial ecosystem.

- Digital inclusion may be promoted by financial inclusion. Promoting access to digital financial services is also a significant factor in digital inclusion, as it ensures that a greater number of individuals can engage in the digital economy. Furthermore, technology plays a significant role in financial inclusion.

Fintech Insights: Top 10 CTOs Of The Fintech Industry

Financial Inclusion: Challenges

Challenges include a lack of infrastructure, low digital literacy, and cultural or social barriers. Data privacy concerns and the risk of overindebtedness also pose significant hurdles. In some areas, limited internet access and high costs prevent people from using digital financial services. Regulatory gaps and bias in financial product design can further hinder progress.

Limited Banking Infrastructure Access

Many rural and distant locations lack banking infrastructure, which hinders financial inclusion. Banks and ATMs are limited in these places, making basic financial services difficult to access. Mobile banking and online payment solutions like PayPal can help close the banking infrastructure gap. Financial service businesses can reach faraway customers without costly branches by using technology.

Poor Financial Literacy

Many people, especially in developing countries, lack financial product and service knowledge, which might hinder financial inclusion. Low financial literacy can prevent people from making educated financial decisions and lead to scams or predatory lending. Governments, NGOs, and financial institutions can work together to create targeted education programs that teach people how to handle their money.

High Financial Services Cost

For low-income people, account upkeep, transactions, and withdrawals are often too expensive. Financial services can be cheaper by encouraging competition and fostering innovative, low-cost products. Additionally, governments should encourage financial firms to offer cheaper products and services to underprivileged groups.

Tight Regulations

Financial services can be challenging for those without formal identification due to strict laws and identification requirements. Refugees, migrants, and the poor are most affected. Governments can improve financial services access by streamlining regulatory processes and allowing more flexible identification. Digital identity systems or community-issued documents may be used.

Social and cultural norms

Cultural and societal conventions can restrict financial inclusion in some societies. Due to gender roles, women in some regions may be discouraged from financial activity. Cultural and social barriers to financial inclusion require focused interventions to raise knowledge, challenge prejudices, and enable marginalised populations to manage their finances. This may involve engaging with community leaders and local organizations to promote change and financial inclusion.

Mistrust of Financial Institutions

People, especially those excluded from the formal financial system, may mistrust financial institutions. Lack of trust can prevent people from using formal financial services, preventing financial inclusion. Financial service providers should prioritize efforts to understand and address underserved populations’ unique needs and concerns, while also working to improve their public image through community engagement and corporate social responsibility initiatives.

Analyzing the Impact of New Regulations and Policies Across Geographies

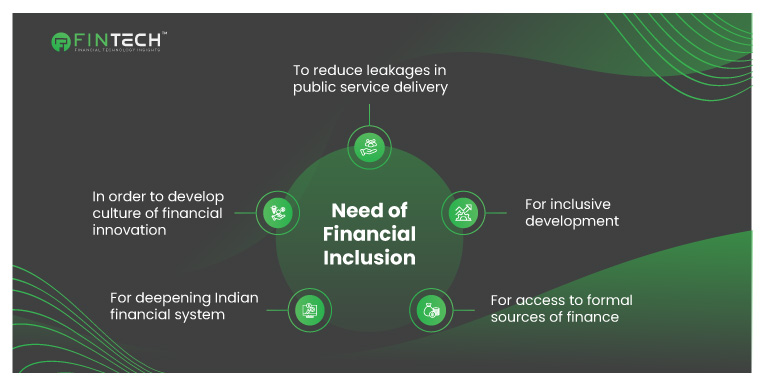

Inclusive growth and economic stability are contingent upon financial inclusion. It has the potential to enhance financial stability when executed responsibly. However, financial stability can be compromised by financial inclusion and credit expansion if they are not properly managed. Three concerns were addressed during this session: How can the financial stability repercussions of financial inclusion and deepening be managed? In order to maximize the social impact of policies, how should decision-makers prioritize them?

The potential of financial inclusion to contribute to economic and financial development, as well as to promote more inclusive growth and greater income equality, is garnering increasing attention. Nevertheless, there is still a great deal to be accomplished, despite the significant progress that has been made. The People’s Republic of China (PRC) and India make up the majority of the 55% of the world’s unbanked adults, which are collectively located in East Asia, the Pacific, and South Asia.

The global pandemic and recent racial and social injustice events have heightened global awareness of inequities and financial instability. They underscore the necessity for financial institutions to establish a global commitment to promote financial inclusion by offering access to affordable and practical financial products and services to address the requirements of the underserved market. According to the Global Findex 1.7 billion adults internationally are unbanked, meaning they do not engage in any basic financial services. While 30 million households in the United States as underbanked, which means they have limited access to fundamental financial services. Consequently, financial services providers are presented with a variety of opportunities to influence change.

Financial inclusion has never been more critical in a world that is becoming increasingly characterized by globalization and digital technology. We can empower individuals to take control of their financial futures and contribute to a more equitable and prosperous global economy by guaranteeing that all individuals, irrespective of their socioeconomic status or geographic location, have access to affordable and appropriate financial products and services. The barriers that impede millions of individuals from obtaining the financial services necessary to enhance their lives and attain economic stability can be overcome through policy reforms, targeted interventions, and innovative solutions.

50 Popular Fintech Companies You Should Know

How CFOs Can Align Regulatory Compliance with Financial Inclusion?

CFOs can design strategies that align business goals with inclusion objectives. They can invest in products for underserved markets, reduce bias in financial services, and collaborate with diverse stakeholders. By prioritizing social impact and measuring progress with clear KPIs, CFOs can drive sustainable growth while addressing financial inequities.

Global C-suite surveys have demonstrated that CFOs prioritized the creation of a positive societal impact when asked to assess and evaluate their business performance. The objective of fostering a positive social impact is a worthwhile endeavor. However, realizing committed, sustainable change depends on how an organization allocates meaningful effort, time, and experience to public well-being—its corporate social purpose. Although it is incumbent upon businesses to generate profits for their shareholders and their organization, a well-defined corporate social purpose can also enhance the organization’s reputation and brand, attract and retain talent, and contribute to improving the communities they serve. This, in turn, assists the organization in attracting socially conscious customers, fostering innovation, and identifying opportunities for profitable development by entering new market segments. The image below has been taken from Deloitte.

FAQ

- Why is financial inclusion important?

Financial inclusion helps reduce poverty, encourages entrepreneurship, and boosts economic growth. It ensures that everyone, including underserved communities, can access financial resources. This inclusion fosters stability, improves quality of life, and helps countries achieve sustainable development goals. Additionally, it opens up opportunities for businesses to serve new markets. - What are the challenges of financial inclusion?

Challenges include a lack of infrastructure, low digital literacy, and cultural or social barriers. Data privacy concerns and the risk of overindebtedness also pose significant hurdles. In some areas, limited internet access and high costs prevent people from using digital financial services. Regulatory gaps and bias in financial product design can further hinder progress. - How does fintech support financial inclusion?

Fintech uses technology to make financial services more accessible and affordable. For example, mobile banking apps, digital payment systems, and micro-lending platforms allow people without traditional bank accounts to manage money. Technologies like AI and blockchain enhance security and efficiency, helping to serve underserved populations better and faster. - What role do regulations play in financial inclusion?

Regulations ensure that financial inclusion initiatives are safe, transparent, and effective. They protect consumers from exploitation, promote fair service access, and encourage innovation. For example, regulations on data privacy ensure that digital financial services respect user rights, while policies promoting fintech growth create opportunities for broader access. - How can CFOs contribute to financial inclusion?

CFOs can design strategies that align business goals with inclusion objectives. They can invest in products for underserved markets, reduce bias in financial services, and collaborate with diverse stakeholders. By prioritizing social impact and measuring progress with clear KPIs, CFOs can drive sustainable growth while addressing financial inequities.

Impact of Fintech on Retail Banking Trends

Conclusion

Financial inclusion is a powerful tool for creating a more equitable and prosperous world. It ensures that individuals, especially those marginalized or underserved, can access essential financial services like savings, credit, and insurance. By empowering people with these resources, financial inclusion drives economic growth, reduces poverty, and promotes innovation. However, its success depends on responsible implementation and alignment with regulatory frameworks. Technological advancements in fintech are revolutionizing how financial services reach underserved populations. Innovations like AI, blockchain, and digital currencies enhance accessibility and affordability. Still, these technologies come with risks, such as data privacy concerns and potential misuse. Addressing these challenges requires balanced policies and a strong commitment to responsible innovation.

Regulations play a critical role in fostering financial inclusion. Regions ensure that inclusion benefits the economy and society by creating an environment where financial services can thrive while protecting consumers. Different geographies face unique challenges, from infrastructure gaps to cultural barriers, but global collaboration can help share best practices and tailor solutions. CFOs and financial leaders are vital in aligning business objectives with financial inclusion goals. Designing inclusive strategies, mitigating bias, and investing in underserved communities can create social impact while driving economic growth. Measuring success through clear KPIs and fostering partnerships with diverse stakeholders are key steps in achieving this balance.

Organizations that prioritize inclusion build trust, attract socially conscious customers, and foster innovation. As we move forward, collaboration between governments, businesses, and technology providers will be essential to overcoming challenges and unlocking the full potential of financial inclusion worldwide.

Read: Fintech in Hospitality: Top 10 Fintech Solutions for Hotels