Let’s talk about fintech and microfinance in this blog. We will be focusing on bridging the Gap for SMEs. The increasing importance of microfinance institutions and fintech partnerships to support small businesses and entrepreneurs in developing regions. How digital lending platforms change access to capital for micro and small enterprises.

What is Microfinance?

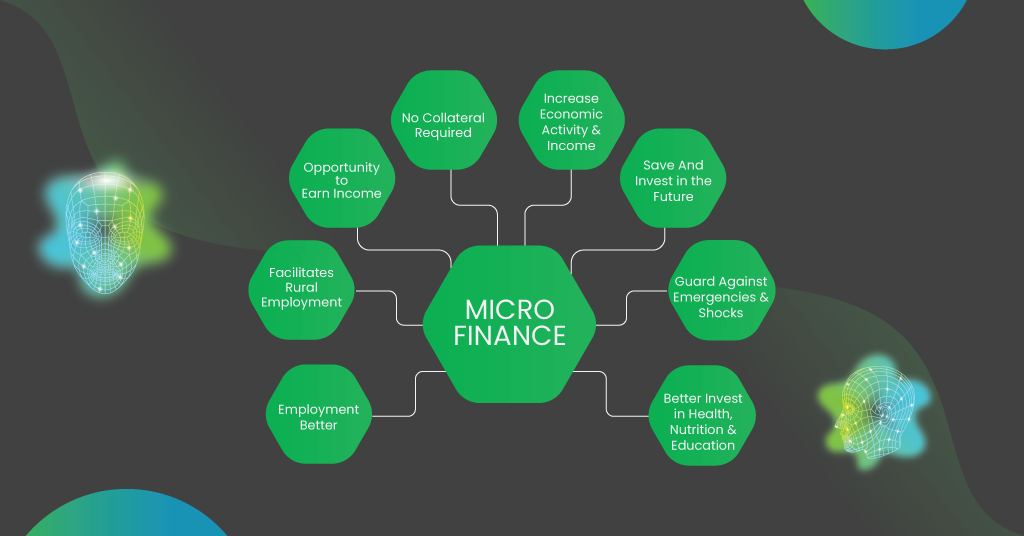

Microfinance, also known as microcredit, is a banking service offered to low-income individuals or organizations that would not otherwise have access to financial services. Microfinance services are offered to individuals who are unemployed or have low incomes, as the majority of those who are poor or have limited financial resources lack the necessary income to conduct business with traditional financial institutions. It is designed to provide essential financial services to individuals who are economically disadvantaged and are unable to access traditional banking services due to their failure to satisfy the criteria established by the majority of lending institutions. The country is home to numerous Microfinance institutions (MFIs) that offer microfinance to individuals who require it.

Microfinance is a financial solution that caters to the financial requirements of low-income individuals and small enterprises frequently excluded from conventional banking systems. Services encompass financial education, insurance, savings accounts, and microloans. Microfinance institutions (MFIs) are essential for the empowerment of marginalized communities, the promotion of entrepreneurship, and the reduction of poverty.

Read: What Is Conversational AI?

SMEs in Developing Regions: An Overview

A joint report by the International Finance Corporation (IFC) and the SME Finance Forum reveals that 65 million enterprises, or 40% of formal MSMEs in developing countries, face an unmet financing need of $5.2 trillion annually- SME Finance Forum

SMEs often operate in rural and semi-urban areas, playing a crucial role in bridging the urban-rural divide. Their presence stimulates local economies, creating a ripple effect on community welfare. SMEs drive innovation by addressing niche market needs and introducing creative solutions. They nurture entrepreneurial ecosystems, enabling individuals to turn ideas into viable businesses.

Small and Medium Enterprises (SMEs) are the backbone of economies worldwide, particularly in developing regions where they are critical in driving growth, employment, and innovation. These enterprises, characterized by their modest scale of operations, are vital for fostering economic resilience and inclusive development. Despite their potential, SMEs in developing regions face unique challenges and opportunities shaped by socio-economic and technological factors.

A multi-stakeholder approach is essential to unlock the full potential of SMEs in developing regions. Governments must simplify regulations, improve infrastructure, and foster a conducive business environment. Financial institutions and fintech companies should innovate tailored financial products to meet SMEs’ unique needs. Investments in digital literacy, skill development, and capacity-building programs are also crucial.

By addressing these challenges and leveraging emerging opportunities, SMEs in developing regions can transition from survival-based entities to growth-oriented enterprises. This transformation will enhance their contribution to local economies and play a pivotal role in global economic resilience and equitable development.

Fintech solutions, such as peer-to-peer lending, digital wallets, and microfinance platforms, address the financing gap, providing SMEs with faster and more flexible access to funds.Integration into global supply chains and participation in regional trade agreements offer SMEs opportunities to scale and diversify their offerings.

SMEs significantly contribute to job creation, accounting for most employment opportunities in developing regions. They provide livelihoods for diverse population segments, including women and youth, fostering social inclusion.

Challenges in the Micro Finance Industry

The microfinance industry has been critical in promoting financial inclusion by providing credit, savings, insurance, and other financial services to underserved populations, particularly in developing economies. Despite its noble objectives and significant achievements, the sector faces various challenges that hinder its ability to maximize impact and scale sustainably. These challenges can be broadly categorized into operational, financial, regulatory, and social dimensions.

The incremental evolution of microfinance is resulting in its transition to a banking-type sector. Clients are striving to obtain substantial credit to expand their economic activities. MFIs must raise capital to satisfy the increasing demand of their clients, as the RBI is establishing stricter CAR norms. We must establish a connection between the market and technologies and the clients. The necessity of this group is indeed expensive, as they are dispersed and typically only utilize small loans. The development of appropriate products for clients remains a significant challenge. Competent human resources are becoming increasingly pressing as the industry expands rapidly to meet the increasing demand.

History of Microfinance

Microcredit was established in 1983 by Bangladeshi social entrepreneur Muhammad Yunus, coinciding with microfinance’s establishment. Grameen Bank was established in Bangladesh by Yunus in 1983. Grameen Bank’s initial objective was to offer entrepreneurs small financing. Yunus’ vision for microcredit was ignited by observing women in Bangladesh who crafted bamboo stools for a mere two cents per day. He determined that the women could increase their margins and generate a more substantial profit if they could take out a loan. The women could repay the loan and maintain their business operation after being issued a $27 loan by the group model.

The aspect of a savings account in microfinance can also be linked to microcredit; creditors may opt to include a loan covenant. The borrower must save a portion of their profits in a savings account with the financial institution as collateral until the loan is paid, as stipulated in the loan covenant. Consequently, it offers creditors some protection, and the borrower would have accrued savings interest on the funds deposited in the savings account if the loan was repaid. Yunus was awarded the Nobel Peace Prize in 2006 for his contributions to Grameen Bank. The bank employs approximately 22,000 individuals and supervises approximately 2,500 operational locations. Additionally, there are 10,000 microfinance institutions in operation at present.

Read: Fintech Marketing: Top 10 Power Strategies to Accelerate Growth

Fintech’s Role in Enhancing Microfinance

1. Digital Onboarding

Fintech simplifies the traditionally cumbersome onboarding process. With mobile-first approaches and biometric authentication, even people in remote areas can easily open accounts and access financial services.

- Fino PayTech (India): Enables rural populations to open bank accounts using biometric verification at local agents.

- Tala (Kenya): Uses a mobile app to provide loans; borrowers only need a smartphone and ID to complete the process.

- Mobile Payments

Mobile payment systems allow users to send and receive money without a physical bank branch, promoting financial inclusion and fostering economic activity.

- M-Pesa (Kenya): Revolutionized payments by providing unbanked individuals access to financial services, allowing users to deposit, withdraw, and transfer money via mobile phones.

- G-Cash (Philippines): Empowers users to pay bills, transfer money, and even secure microloans through their mobile phones.

3. Credit Scoring with AI

To assess creditworthiness, Fintech platforms use advanced algorithms and alternative data sources (e.g., phone usage, e-commerce activity, utility payments, and social media behavior). This approach enables microfinance institutions (MFIs) to offer loans to underserved populations who lack traditional credit histories.

- Branch International: Uses smartphone metadata, like SMS records and call history, to assess loan eligibility.

- Lenddo: Employs AI to analyze social media profiles and online behavior for credit scoring.

4. Reduced Operational Costs

Automation and digital platforms streamline operations, reducing administrative and overhead costs. Lower costs mean MFIs can pass the savings on to their customers through affordable interest rates or expanded services.

- GramCover (India): Offers rural insurance services digitally, reducing field agent dependency and operating costs.

- Musoni Systems: A cloud-based core banking system specifically designed for MFIs to improve efficiency and reduce manual processes.

5. Enhanced Transparency

Blockchain technology promotes secure, tamper-proof records of transactions, minimizing fraud and increasing trust between lenders and borrowers.

- BanQu: Provides blockchain-based financial identities for unbanked individuals, enabling transparent transaction histories.

- Moeda (Brazil): Leverages blockchain to track microloans and ensure that funds are used for their intended purpose.

Additional Impacts of Fintech in Microfinance

- Peer-to-Peer Lending: Platforms like Kiva connect individual lenders with borrowers globally, enabling microloans that bypass traditional financial institutions.

- Financial Literacy Tools: Apps like Kubo Financiero integrate financial education into their services, ensuring borrowers understand loan terms and repayment structures.

- Insurance Access: Companies like BIMA offer microinsurance through mobile phones, protecting low-income individuals from unexpected financial shocks.

Empowering Small Businesses: The Growing Role of Microfinance and Fintech Partnerships in Developing Regions

Small businesses are the backbone of many developing economies, yet they often face significant challenges in accessing credit and financial services. Microfinance institutions (MFIs) and fintech partnerships are increasingly playing a transformative role in bridging this gap, empowering entrepreneurs, and fostering economic growth in underserved regions.

1. The Role of Microfinance in Supporting Small Businesses

Microfinance provides small, affordable loans and other financial services to individuals and businesses that traditional banks typically overlook. It has become a critical tool for fostering entrepreneurship and alleviating poverty.

- Access to Capital: Small loans help microentrepreneurs start or expand their businesses, purchase equipment, or manage inventory.

- Tailored Solutions: MFIs often understand local markets better and provide personalized loan terms that align with borrowers’ needs.

- Capacity Building: Many MFIs offer financial literacy programs and mentorship, enabling small business owners to make informed decisions.

2. Fintech Partnerships: Revolutionizing Microfinance

Fintech partnerships are accelerating the reach and efficiency of microfinance by leveraging technology to address traditional barriers:

- Digital Platforms: Mobile apps and online platforms simplify the loan application process, reducing paperwork and increasing accessibility for rural entrepreneurs.

- Data-Driven Lending: Fintechs utilize alternative data, such as transaction histories, mobile phone usage, and e-commerce records, to assess creditworthiness and expand financial inclusion.

- Real-Time Transactions: Mobile wallets and digital payment systems allow borrowers to access funds and repay loans seamlessly, reducing operational costs for MFIs.

- Automation and AI: AI-powered tools help streamline processes like credit scoring and fraud detection, enabling faster and more accurate decision-making.

3. Benefits of Microfinance and Fintech Collaboration

- Increased Financial Inclusion: The combined efforts of MFIs and fintechs provide small businesses with the tools they need to access formal financial systems.

- Scalability: Technology allows microfinance services to scale rapidly, reaching more entrepreneurs in remote and underserved areas.

- Lower Costs: Fintech innovation reduces the cost of loan disbursement and repayment, making microfinance more sustainable for institutions and affordable for borrowers.

- Enhanced Risk Management: Advanced analytics and AI models help predict defaults and improve portfolio quality.

The Impact of Digital Lending Platforms on Micro and Small Enterprises

1. Breaking Traditional Barriers

Digital lending platforms address the challenges MSEs face with conventional financial institutions:

- Minimal Documentation: Unlike traditional banks, digital lenders require fewer documents, simplifying the loan application process.

- Alternative Credit Assessment: These platforms use alternative data, such as mobile phone usage, e-commerce sales, and transaction histories, to assess creditworthiness for borrowers with limited credit histories.

- Faster Processing: Automation enables quicker loan approvals and disbursements, ensuring businesses can meet urgent capital needs.

2. Technology-Driven Lending Models

- AI and Machine Learning: Advanced algorithms analyze borrower data to predict credit risk, customize loan offerings, and reduce default rates.

- Mobile Integration: Mobile apps enable entrepreneurs to access loans, monitor repayments, and manage accounts seamlessly, even in remote areas.

- Blockchain for Transparency: Blockchain ensures secure, tamper-proof records of loan agreements and repayment histories, fostering trust between lenders and borrowers.

Case Studies: Success Stories of Fintech and Microfinance Collaboration

1. M-Pesa and Microfinance in Africa

M-Pesa, a mobile money platform launched in Kenya, has become a cornerstone of financial inclusion in Africa. By enabling users to send and receive money, pay bills, and access microloans through their mobile phones, M-Pesa has empowered millions of unbanked individuals. The platform’s collaboration with MFIs has expanded its impact, allowing borrowers to receive and repay loans digitally.

2. Grameen Foundation and Digital Tools

The Grameen Foundation leverages fintech solutions to enhance its microfinance operations. Digital financial services, mobile apps, and data analytics tools have improved service delivery and enabled the foundation to reach remote communities efficiently.

3. Kiva’s Blockchain Integration

Kiva, a global microfinance platform, utilizes blockchain technology to create a secure and transparent credit infrastructure. This innovation reduces duplication and ensures accurate credit histories for borrowers, facilitating better access to financial services.

Read: Impact of Fintech on Retail Banking Trends

The Future of Fintech and Microfinance

The global economy’s landscape is being transformed by the convergence of financial technology (fintech) and microfinance, empowering underserved populations and promoting financial inclusion. This synergy unites the community-centric approach of microfinance with the technological advancements of fintech, thereby facilitating the development of innovative solutions to long-standing challenges in financial accessibility, affordability, and efficiency.

AI-Powered Financial Tools: Driving Efficiency and Inclusion

Artificial intelligence (AI) is at the forefront of this transformation, reshaping how financial services are delivered. AI-powered tools enhance credit scoring by analyzing non-traditional data such as mobile usage patterns, social media activity, and geolocation data. This shift allows lenders to assess creditworthiness more accurately, especially for individuals lacking conventional credit histories.

AI also improves fraud detection by leveraging machine learning algorithms to identify real-time anomalies and suspicious activities. This ensures the security and trustworthiness of transactions, a critical factor in microfinance operations where trust is paramount. Moreover, AI enables the personalization of financial services, tailoring solutions to the unique needs of individuals and communities. Personalized services, such as customized loan products or savings plans, enhance user engagement and financial literacy, contributing to the long-term success of microfinance initiatives.

Decentralized Finance (DeFi): Redefining Lending and Borrowing

Blockchain-based Decentralized Finance (DeFi) platforms are disrupting traditional financial models by offering new avenues for lending and borrowing without intermediaries. These platforms utilize smart contracts to facilitate transactions, reduce costs, and increase transparency. For microfinance institutions, adopting DeFi technologies can streamline operations, enabling them to reach more clients at lower costs.

DeFi also empowers borrowers by giving them direct access to global financial markets. This can be particularly transformative in regions with limited access to formal banking services. For example, individuals in rural areas can secure loans or invest their savings without relying on traditional banks, thus fostering economic independence and resilience. Additionally, using stablecoins in DeFi ecosystems mitigates currency volatility risks, ensuring the stability of funds for borrowers and lenders alike.

Sustainability Initiatives: Promoting Green Microfinance

As global attention shifts toward environmental and social goals, fintech solutions increasingly align with sustainability initiatives. Green microfinance programs, supported by digital platforms, are emerging as a powerful tool to promote eco-friendly practices. These programs provide financial resources to support renewable energy adoption, sustainable agriculture, and climate-resilient infrastructure.

Fintech platforms also facilitate the monitoring and reporting of environmental impacts, ensuring transparency and accountability. By integrating Environmental, Social, and Governance (ESG) metrics into financial products, these initiatives attract impact investors and encourage responsible lending. This alignment addresses climate change and supports community development, creating a ripple effect of positive social and environmental outcomes.

Bridging Financial Gaps: Empowering Communities

The collaboration between fintech and microfinance promises to bridge persistent financial gaps, empowering individuals and communities worldwide. Mobile-based microfinance platforms enable users to access credit, savings, and insurance services with a few taps on their smartphones. This accessibility is particularly crucial in regions with sparse or nonexistent physical banking infrastructure.

Moreover, digital platforms facilitate financial literacy programs, equipping users with the knowledge and skills needed to manage their finances effectively. By fostering financial independence, these initiatives contribute to poverty alleviation and economic stability.

Fintech Insights: Top 10 CTOs Of The Fintech Industry

Conclusion

A transformative transformation has occurred in the financial landscape, particularly in the fintech sector, due to the emergence of technology. Traditional paradigms have been reshaped by financial technology, or fintech, which has paved the way for innovative solutions in the banking and finance industry. The synergy with microfinance, a discipline dedicated to providing financial services to underserved populations, is one of its most significant contributions. This article examines the intersection of fintech and microfinance, examining how this partnership accelerates global financial inclusion and revolutionizes access to financial services.

By integrating technology with inventive financial solutions, digital lending platforms are revolutionizing access to capital for micro and small enterprises. In addition to addressing the credit divide, they foster a more resilient and inclusive financial ecosystem. The full potential of these platforms will be unlocked by addressing challenges such as digital literacy and regulatory compliance as they evolve. In doing so, digital lenders can enable MSEs to advance economic progress and transform local communities globally. Fintech and microfinance are potent allies in the pursuit of financial inclusion. Microfinance institutions can expand their scope, overcome traditional barriers, and serve as catalysts for socio-economic development by utilizing technology. Innovation is not the only benefit of the synergy between these sectors; it also promotes a more inclusive financial ecosystem where opportunities are available to all, irrespective of their economic status.

Read: Top 10 FinTech Cybersecurity Challenges in 2025

We will be back with more exciting articles in the fintech domain!

Write to us for any suggestions.