One of the most significant challenges that really marked the compliance issue for the fintech industry all over the world was the year 2025. Fintech companies are being forced to comply with an increasingly complex and rapidly changing set of regulations as financial ecosystems become more sophisticated and regulators become more stringent. Nevertheless, the fact remains that manual operations are not able to keep up with the rapid growth of fintechs at the speed they are growing. This is the point at which Regulatory Technology (RegTech) comes to the rescue.

Financial crime prevention (AML), customer identification programs (KYC), global data privacy regulations, and even the emergence of DORA and MiCA as compliance requirements have transformed compliance into a recurring theme of leadership discussion rather than a discussion on ticking off the boxes. It is changing the way fintechs comply with regulatory requirements while maintaining innovation, productivity, and expansion.

The Compliance Crunch in Fintech

For many years, Fintech innovation has been quicker than regulation. However, by 2025, the difference between the two has become considerably smaller. But the narrowing is not in favor of most startups. Regulators worldwide have caught up and are now imposing stricter oversight and heavier fines. In Fenergo’s Global Financial Institution Fines Report 2025, it is stated that the total penalties for AML and KYC failures exceeded $1.23 billion all over the world, which is 18% more than in 2023.

Fast-expanding fintechs will face a drastic situation because of this. Every new market entry means a bundle of different local regulations, which turns compliance into a constantly changing target. Besides that, as financial crime becomes more complicated, even the best-established fintechs are finding it hard to keep control.

They continue with manual audits, fragmented systems, and also human-dependent monitoring. These are methods that are no longer effective. Fintechs have realized that they require intelligent, automated systems that eventually can grow at the same rate as their products, not slower. This is exactly the point at which RegTech is facilitating a change in compliance from being reactive to proactive.

Why RegTech Matters Now More Than Ever

Regulatory Technology, or RegTech, is basically the application of cutting-edge technologies. Such technologies are Artificial Intelligence (AI), Machine Learning (ML), Blockchain, and API integrations. Further, these technologies were used to automate, streamline, and make regulatory compliance more efficient.

The idea is old, but its role in the fintech sector has been increasing at an incredible speed during the last few years. According to a 2024 study conducted by Juniper Research, the worldwide expenses in RegTech will go beyond $28 billion by 2026. Eventually, this will be a result of the huge demand for automation, real-time processing of data, and compliance with cross-border requirements.

Essentially, RegTech equips fintechs with tools to handle enormous regulatory data, spot risks early, and secure routine compliance with both local and global laws. Different from the conventional compliance software, contemporary RegTech instruments are all cloud-based, highly flexible, and have the ability to learn from behavior and transactions. They are making compliance an always-present, smart function rather than something that is done periodically and superficially. RegTech, in 2025, just when the fintech sector is under great scrutiny, is like the operational backbone.

The Compliance Challenges Fintechs Face in 2025

The increasing size of fintech companies brings along with it a regulatory burden that is more and more complicated. The problems that the companies face are no longer only that they have to understand new laws. They also have to handle the volume, speed, and changes of the compliance data. Some of the biggest challenges are those outlined below:

1. Multi-Jurisdictional Compliance

It is a common pattern for fintech companies to grow quickly in different markets. However, each regulatory body, for example, the U.S., Singapore, or the EU, implements a different set of rules. Without the help of machines, it is impossible to deal with all these interrelated components simultaneously, which can lead to delays and, consequently, the risk of errors increases.

2. Real-Time AML and KYC Demands

The number of online transactions and the use of digital onboarding methods have led to an increase in fraud. This has made fraud prevention more complex. Evidently, to identify deviations at a very high speed, continuous KYC and real-time transaction monitoring have become mandatory, something that can hardly be accomplished by manual teams.

3. Data Privacy and Security

Worldwide data protection regulations like GDPR, CCPA, and the EU’s Digital Operational Resilience Act (DORA) have led to an obligation for fintech firms to implement data-handling systems that are transparent, traceable, and safe.

4. Reporting and Audit Overload

With the development of fintech, so does the number of regulatory reports that have to be filed. Manual reporting not only slows down submissions but also risks that the reports will not be consistent, thus triggering compliance reviews or penalties. All these problems are signaling the same answer to us. That is the use of automation through RegTech.

How RegTech Is Scaling Compliance for Fintechs

RegTech’s impact lies in its ability to replace repetitive manual tasks with intelligent, automated systems. Here’s how fintechs are leveraging it to scale compliance efficiently and effectively:

1. Automated KYC and AML Verification

AI-powered RegTech platforms can verify customer identities in seconds using biometric data, digital document verification, and cross-database matching. For instance, fintechs like Trulioo and Onfido enable instant verification while adhering to global AML standards.

This automation significantly reduces onboarding time. Because of this, costs are cut by up to 70%, according to Deloitte’s RegTech for Fintechs Report 2025. More importantly, it enhances user experience by making compliance invisible to the end user.

2. AI-Driven Risk Scoring and Fraud Detection

Modern RegTech platforms utilize machine learning to identify suspicious transactions before they escalate into threats. By analyzing transaction histories, behavioral data, and network connections, they can assign dynamic risk scores to each account or activity.

For example, ComplyAdvantage employs predictive analytics to detect unusual money flows across regions. Reducing false positives and improving investigation accuracy.

3. API-Based Integrations

APIs are at the heart of scalable RegTech. They enable seamless integration with payment systems, CRM tools, and banking cores, allowing compliance data to flow in real time. Fintechs like Stripe use API-driven compliance infrastructure to ensure global consistency across 40+ countries.

4. Automated Reporting and Regulatory Intelligence

Gone are the days of manually preparing compliance reports. Tools like Clausematch and Ascent RegTech automate documentation, reporting, and policy updates based on regulatory changes.

This real-time intelligence means fintechs no longer have to wait for auditors to catch issues — they can self-correct instantly.

Case Studies: RegTech in Real-World Fintechs

Revolut:

In 2025, Revolut expanded into multiple markets, including Latin America and Asia-Pacific. To manage regulatory variation, the company partnered with AI-driven RegTech vendors to automate AML screening and sanction checks. The result? A 35% improvement in compliance efficiency and faster customer onboarding.

Stripe:

With operations spanning dozens of countries, Stripe uses embedded RegTech APIs for local compliance. That too, from tax reporting to AML verification. These integrations allow it to meet regional standards instantly, supporting global expansion without additional compliance teams.

N26:

The European challenger bank leverages RegTech solutions to maintain compliance with the EU’s stringent data privacy and digital operational laws. This automation has allowed N26 to focus more on innovation while maintaining strong regulatory alignment.

The Measurable Benefits of RegTech Adoption

RegTech is not only a defensive investment; it is a differentiator that sets a company apart from its competitors. Basically, it is reshaping the business landscape of fintechs in the following ways:

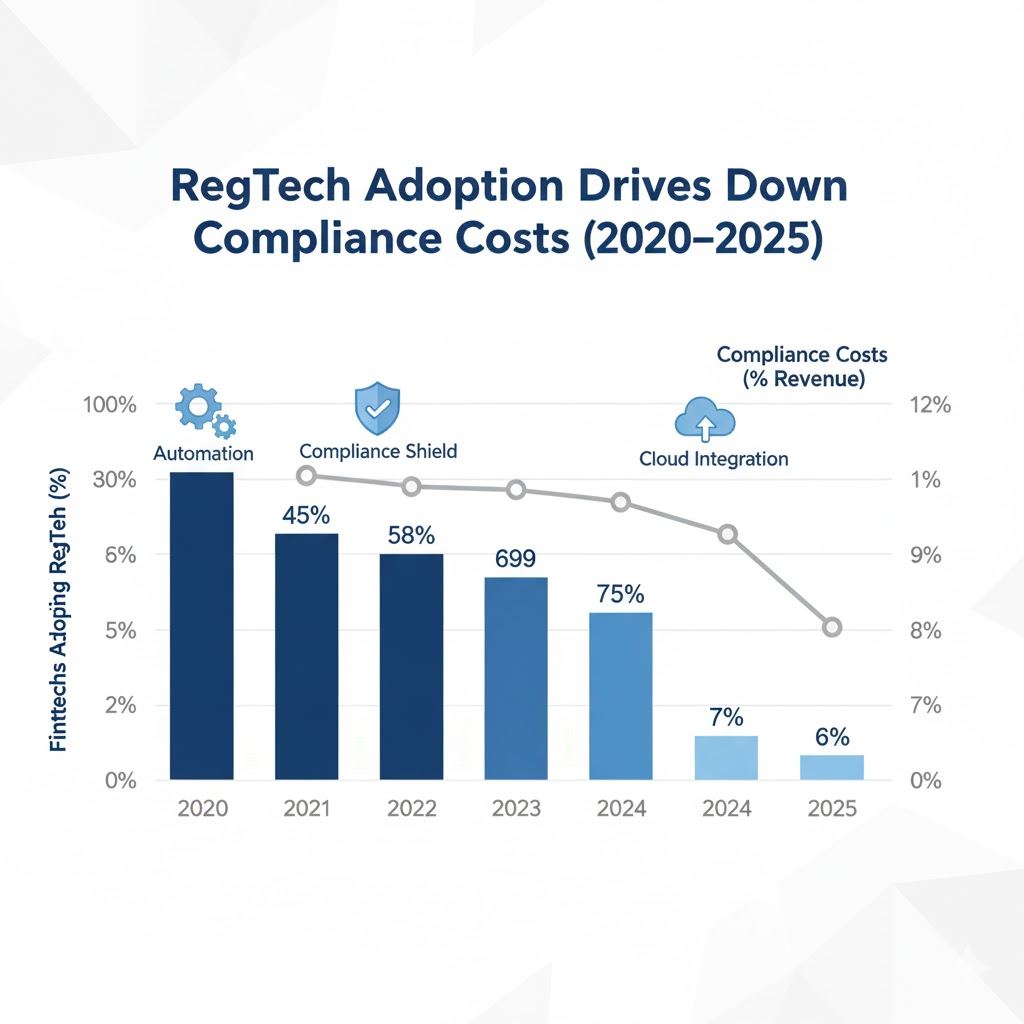

Money-saving: It is estimated that the task of compliance can be automated, and the operational costs can be halved. The report published in 2024 by Allied Market Research reveals that fintechs that have adopted RegTech have been able to decrease the compliance-related expenses by as much as 40%.

Quick Entry into New Markets: Automated regulatory checks and real-time reporting enable fintech companies to move into different geographical areas without delay and without the risk of non-compliance.

Customer Trust: Transparent and secure procedures lead to increased confidence on the part of the users. This trust is very important in customer retention in the field of finance.

Improved Risk Management: Predictive models allow companies to identify areas where fraud might occur and take measures to prevent it before it happens. Thus, the company will be faced with fewer fines and less damage to its reputation.

Ability to Scale: The RegTech solutions installed today will be compatible with the company’s future growth and, therefore, the compliance level will be able to keep up with business expansion.

The Future of RegTech in Fintech Compliance

The future of compliance is intelligent, predictive, and embedded. By late 2025, the evolution of RegTech will be shaped by three major trends:

1. Predictive Compliance through AI

Instead of waiting for audits or anomalies, fintechs are using predictive AI to identify potential risks before they occur. These models analyze trends, past violations, and evolving regulatory language to suggest preventive measures.

2. Compliance Clouds and Industry Collaboration

A growing number of fintechs are joining compliance cloud ecosystems. Shared infrastructures where data, risk models, and regulatory updates are standardized. This collective intelligence is helping smaller players achieve compliance at par with large institutions.

3. Regulator-Fintech Partnerships

Regulators themselves are embracing technology. The UK’s Financial Conduct Authority (FCA) and Singapore’s MAS now use supervisory technology (SupTech) to interact with fintech data in real time. This two-way digital relationship makes compliance faster, more transparent, and less adversarial.

According to Gartner’s 2025 Fintech Outlook, by 2027, 90% of fintechs will rely on RegTech platforms for regulatory and governance management. It marks a shift from manual oversight to intelligent automation.

Conclusion

RegTech doesn’t just protect fintechs from regulatory scrutiny; it empowers them to innovate freely, expand globally, and build trust sustainably. By integrating intelligent automation, fintech companies can transform complex compliance processes into streamlined, scalable systems that drive resilience and reputation.

As financial ecosystems continue to digitize, the partnership between fintechs and RegTech providers will define who scales safely and who struggles to stay compliant. The future of fintech is not just digital. It’s regulatorily intelligent. And RegTech is leading that transformation.

FAQs

1. How can fintechs pick the right RegTech partner?

Focus on scalability, data security, and regional expertise. Run pilot tests to ensure smooth integration before a full rollout.

2. Can RegTech replace human compliance teams?

No. It automates workflows, but human oversight is vital for judgment, ethics, and regulatory interpretation.

3. What challenges do fintechs face with RegTech adoption?

Integration, data privacy, and regulatory complexity are common. A phased rollout and team alignment help ease adoption.

4. How does RegTech help fintechs operating globally?

It automates jurisdictional rules, updates regulations in real time, and ensures compliance across multiple regions.

5. What ROI can fintechs expect from RegTech?

Firms using RegTech see up to 40% lower compliance costs and 25% faster onboarding, boosting efficiency and trust.

To participate in our interviews, please write to us at sudipto@intentamplify.com