You must have used Razor Pay, PayPal, Amazon Pay, Google Pay, Apple Pay, or Zelle!

Let’s discuss the future of digital wallets and payment systems for the unbanked, which includes the rise of mobile money, digital wallets, and other alternative payment systems in emerging markets. We will also highlight how fintech is reducing transaction costs and expanding access to essential financial services.

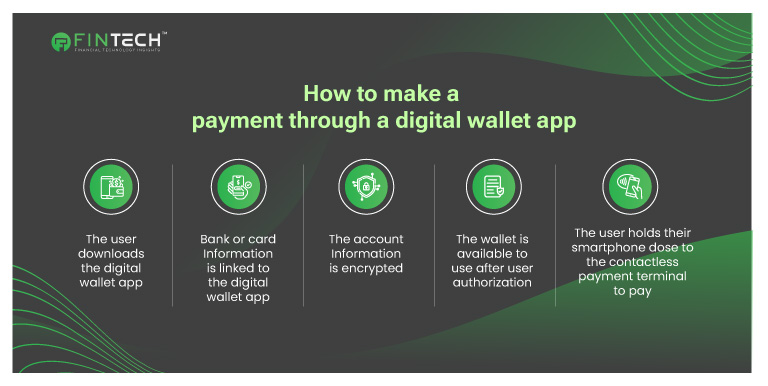

What Are Digital Wallets?

85% of global consumers have used at least one emerging payment method, while 93% are likely to use an emerging payment method in the next year.

A digital wallet, also called an e-wallet or online wallet, is a software-based system or application containing various payment information, including credit card details and bank account information. This enables the execution of electronic transactions.

It functions as a conduit between the digital realm and conventional payment methods, enabling the seamless execution of transactions via smartphones, laptops, or other connected devices. Consider it a digital version of your physical wallet with improved security measures and functionalities.

Fintech Insights: Top 10 Strategies for Effective Fintech Branding

The Rise Of Mobile Money

The widespread proliferation of smartphones and enhanced internet access has facilitated the digital payment revolution. A seamless payment experience is becoming increasingly popular among consumers, who are adopting mobile wallets, UPI, QR codes, and mobile point-of-sale systems.

Noncash retail payment transactions grew 13% globally and 25% in emerging nations between 2018 and 2021. Emerging markets in Africa (Morocco, Nigeria, and South Africa) and Asia grew quickest. Some emerging markets are forecast to increase 15% between 2021 and 2026.

Four important phenomena have boosted digital payments. Consumers’ migration from cash to contactless digital payments was expedited. Second, global e-commerce volumes rose 25% between 2019 and 2020 and are predicted to expand 12–15% year until 2025. Third, the government pushes for cashless payments to improve interoperability, tax leakages, and assistance distribution hastened the adoption of new digital payment systems, including Wave in the Central African Republic, UPI in India, and Pix in Brazil. Finally, investors’ interest in digital payments rose, spurring payments-focused fintechs. These corporations provided 40% of Africa’s $5.2 billion digital start-up finance in 2021.

Fintech Insights: Top 10 CTOs Of The Fintech Industry

Major Players

- MoneyGram International

- Apple

- Mastercard

- Alibaba Group Holding Limited (China)

- PayPal

- Samsung Electronics Co., Ltd. (South Korea)

- Visa

- Tencent Holdings Ltd (China)

- Amazon.com, Inc. (U.S.)

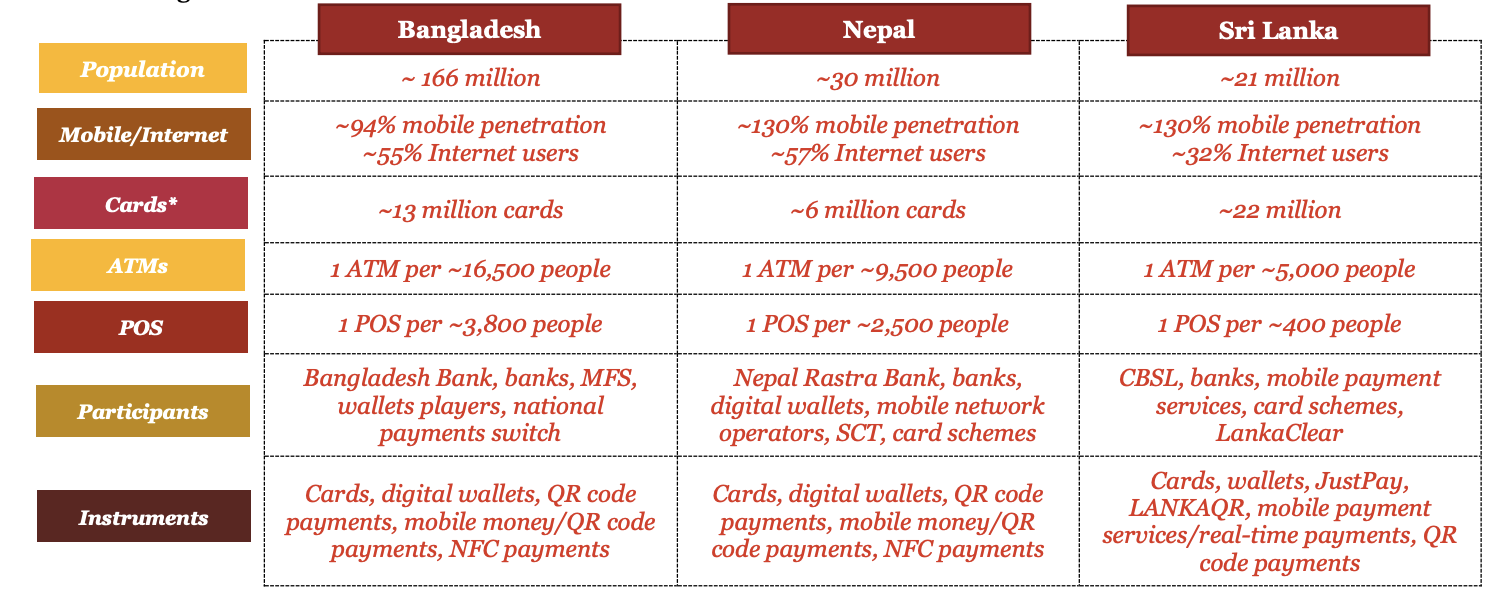

Alternative Payment Systems In Emerging Markets

The graphic below has been taken from PwC.

- Cryptocurrencies: In regions with volatile local currencies, cryptocurrencies provide an alternative for storing and transferring value. Platforms like Bitcoin and Ethereum are gaining traction among users who lack access to traditional banking.

- QR Code Payments: Simple and cost-effective, QR code-based systems like Alipay and WeChat Pay are popular in Asia, allowing users to make payments via scanned codes.

- Agent Networks: In rural areas, agent networks act as intermediaries, enabling cash-in and cash-out transactions for digital wallets. This model has been successful in countries like Bangladesh and the Philippines.

- Blockchain: Blockchain technology is being leveraged to create transparent and low-cost cross-border payment systems, reducing reliance on traditional remittance channels.

50 Popular Fintech Companies You Should Know

How Fintechs Are Reducing Transaction Costs And Expanding Access To Essential Financial Services?

- Payments made through contactless technology: NFC technology is utilized in contactless payments, which allows users to make NFC mobile payments by swiping their smartphone or smartwatch on NFC-enabled payment terminals.

- Recharges and bill reimbursements: With just a few clicks, digital wallets allow you to recharge mobile phones, pay utility expenses, and top up other services.

- Peer-to-peer (P2P) transfers: The necessity for conventional cash or cheque transfers is eliminated by the ability to transfer funds to friends and family instantaneously.

- Rewards and loyalty badges: Numerous wallets incorporate loyalty programs, which enable users to accumulate rewards points and discounts for future purchases.

- Tracking expenses: Digital wallets frequently provide the ability to monitor spending patterns and organize expenses, thereby facilitating the management of your finances more efficiently.

- Security: Biometric authentication, multi-factor authentication, and tokenization techniques enhance the security of digital wallets, thereby decreasing the likelihood of fraud.

- Cross-border transactions: Cross-border transactions and currency conversions are supported by certain wallets, facilitating global transactions for businesses and travelers.

Digital Wallets And Payment Systems For The Unbanked

The unbanked refers to individuals who lack access to a bank account or financial institution. According to the World Bank, nearly 1.4 billion adults globally remain unbanked. Factors contributing to this include lack of documentation, high banking fees, geographical barriers, and mistrust of financial institutions. The unbanked often rely on cash transactions, making them vulnerable to theft and limiting their access to formal financial services such as credit, insurance, and savings.

Several payment systems are specifically designed to cater to the needs of the unbanked. These include:

- M-Pesa: Originating in Kenya, M-Pesa is one of the most successful mobile money services globally. It allows users to send and receive money, pay bills, and access microloans without a bank account.

- Paytm: Widely used in India, Paytm combines digital wallets with a range of services like bill payments, shopping, and ticket booking, empowering unbanked users to participate in the digital economy.

- Airtel Money: Operating in several African countries, Airtel Money facilitates money transfers, bill payments, and merchant transactions for users without access to traditional banking.

Conclusion

The manner in which we pay has been transformed by digital wallets, which provide unparalleled security, efficiency, and convenience. We can anticipate that digital wallets will become even more ingrained in our daily lives as technology continues to evolve, influencing commerce’s future.

Digital wallets and payment systems can potentially bridge the financial inclusion gap for the unbanked. By leveraging technology, these solutions can empower individuals to participate in the formal economy, improve their financial resilience, and ultimately uplift communities. However, achieving this requires concerted efforts from governments, businesses, and non-profit organizations to address existing barriers and foster an inclusive digital ecosystem.

Read: Fintech in Hospitality: Top 10 Fintech Solutions for Hotels