Banks have found payment data indispensable for developing their marketing plans and attracting high-value clients.

Financial institutions are now faced with rapid change in the financial sector, and traditional mass advertising doesn’t always yield the expected results. Banks need to be much more focused on finding, engaging, and converting their valuable targets. Payment data provides banks with valuable insights into customer behaviors, spending patterns, and customer needs.

These insights can be applied to account-based marketing (ABM). Using payment data enables marketing teams to identify, engage, and convert their most valuable targets with greater accuracy than ever before.

Unlike demographic profiling, which provides historic trends, payment data exposes banks to actual, real-time customer behavior and activity.

This means that banks can better observe and respond to emerging opportunities.

The non-linear path of customers to decisions means that a surveillant observer can detect changes, such as a business ramping up supplier payments or a customer indicating interest in a particular category, and act before they fully rationalise their intention or, ideally, at the point of purchase.

Payment data can augment these signals so marketers can prepare and communicate relevant offers, content, and engage with the person who is the decision-maker, with appropriate timing.

The Strategic Value of Payment Data for Banks

Payment data is more than a record of transactions; it’s a unique, proprietary asset that allows banks to be more strategic and deeper with their customers.

The real power is that banks can see real-world behavior and emerging consumer needs as they happen through transactions on the backend. That level of visibility into customer behavior is unmatched by other data sources or data types.

Unique qualitative levels of insight:

- High definition data: Payment records provide the specifics of what, when, how often, and how much an individual purchased.

- Clarity of behavior: This data reflects actual consumer and business behavior as opposed to derivatives based on demographics or third-party data.

- Utility of proprietary data: Because payment data belongs to the bank, it allows for segmentation and personalization based on exclusive behavior.

Behavioral and Real-Time Targeting

- Instantaneous signals: Whether it is an increase in payments to a supplier or a new pattern of spending, these signals emerge in real-time.

- Timely engagement: Banks can act quickly to deliver very precise offers or outreach when it is most relevant.

- Dynamic targeting: Campaigns can be adjusted in real-time, based on live transactions, not on stale snapshots.

As per J.P. Morgan’s 2025 Investor Day Transcript, they process over $10 trillion and nearly 60 million transactions in payments every day.

The Importance of Payment Data in Account-Based Marketing (ABM)

For banks, account-based marketing has progressed from human trials to high-value clients through targeted outreach.

The opportunity, however, is ensuring you have targeted the right accounts with the right messaging at the right time. This is precisely where payment data turns ABM from a strategy that relies on sweeping generalizations and aims for plausible, actionable insights that are fact-based.

Payment data provides an unparalleled view of the commercial and personal financial behaviour of clients.

Rather than relying on standard demographic or industry data sources, payment data can provide real-time transaction data: who a business spends money with (the vendors), their spend seasonality, and triggers of growth, distress, or changing priorities.

When utilized in ABM workflows, payment data allows marketing teams to identify prospective opportunities and custom-tailor campaigns with precision.

Precision Targeting of High-Value Accounts

One of the most effective applications of payment data within ABM (account-based marketing) is to determine which accounts will likely deliver enterprise value in the long run.

Patterns in transaction records can illustrate growth in:

- Changes in revenue over time – e.g., a consistent rise in incoming payments from new customers.

- Changes in operations – such as an increase in payroll or supplier payments.

- New geographical areas – e.g., payments to vendors in new parts of the country, or new countries altogether.

All of these trends allow banks to more effectively prioritize the time and effort of outreach to the high-value accounts. Such accounts are either scaling or experiencing a transition, thus, are at the point of highest interest in terms of new financial products or services.

Indicators of Buying Signals

In traditional marketing, intent data often comes from the familiar situations of “visiting our website”, or “going to congress, and downloading content. In banking, however, payment activity is far more indicative of intent. For example:

- A spike in payments overseas could indicate the need for FX solutions.

- A sizeable, irregular transaction could indicate a capital investment requiring financing.

- A rise in the number of small-ticket payments could indicate increased e-commerce activity and potential for merchant services.

These signals help marketing teams to align offers with an actual or intended business. It makes their outreach far more contextual and identifiable.

Mapping The Account Lifecycle

Payment data also supports lifecycle marketing by showing where an account sits in its lifecycle with the bank.

For instance, if a new client joins with some basic services, they may move into cash management, then lending, and then treasury.

By understanding transaction trends, banks will know when a client is ready for a new product presentation without guessing or waiting until the client asks for it.

Enabling Hyper-Personalized Messaging

An effective ABM strategy is more than identifying the right accounts; it requires speaking the language of each account.

Payment data empowers marketers to build messaging based on actually demonstrated client behaviors (not assumptions):

- Referencing industry-specific trends, including agricultural spending dynamics or construction payments, depending on the recurring and cyclical nature of the spending.

- Indicating relevant solutions based on the transaction mix – supply chain solutions or payment automation, for example.

- Adapting value proposition messaging based on the trajectory of the business or even operational challenges evidenced in transaction behavior.

By linking the subject of the campaign to a client’s financial reality, banks can demonstrate true empathy – a clear sign of trust and credibility.

Maximizing Timing in the Campaign

Timing has critical importance in the context of ABM. Accessing payment data in near real time allows a bank to add value to a client’s experience when they are most likely to engage.

For example, outreach based on payment data for a significant business expansion payment could showcase available working capital solutions at the time the client’s need is the greatest.

Timing with payment data in ABM might be the difference when trying to convert a client from a prospect into a deal.

In what has become an increasingly competitive marketplace in financial services, ABM driven by payment data provides a significant advantage over the competition.

ABM replaces assumptions with data, saves wasted spend on marketing, and supports a bank in being viewed as a partner in the growth of their clients.

Banks that embed payment data in their ABM must not only be reactive to a client’s requests and needs, but they will often have anticipated those requests and needs before the client has even become aware of the growth opportunity. It is this level of sophistication that separates leading institutions from the rest of the market.

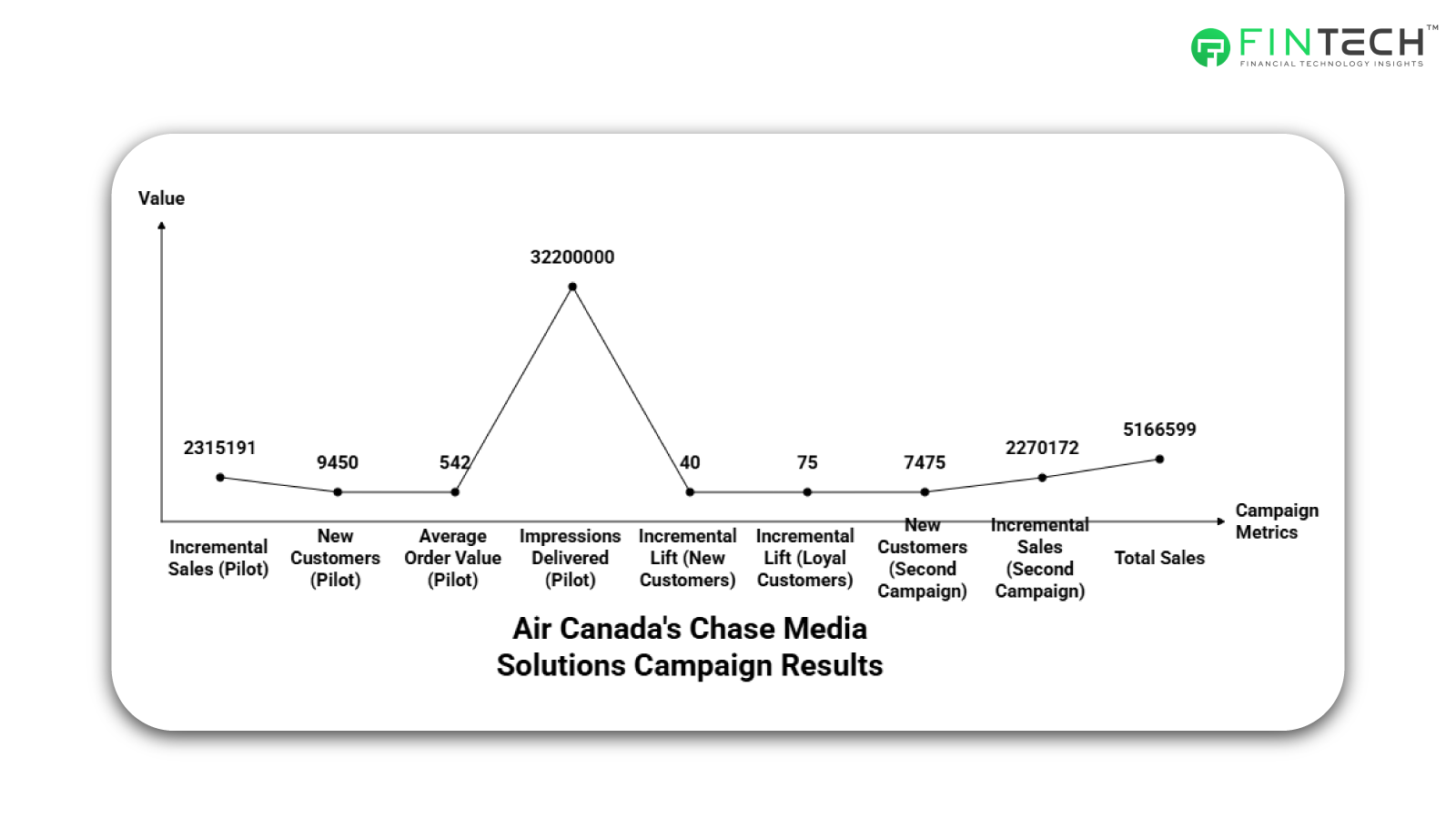

Real-World Use Case: Air Canada’s Chase Media Solutions Campaign

Overview

Air Canada partnered with Chase Media Solutions to engage in transaction-based marketing to effectively produce incremental ticket sales to Chase’s U.S. cardholders.

Campaign Mechanics

Chase used its purchase data to identify cardmembers who had not made any purchases on Air Canada tickets in the past year.

Together, Chase and Air Canada created an offer for cashback with a minimum spend requirement to incentivize cardholders to purchase more tickets rather than ancillary spending such as upgrades and baggage fees.

Results from a 30-Day Pilot Phase

- Incremental Sales: $2,315,191 (accounting for a 45% lift among new customers)

- New Customers Acquired: 9,450

- Average Order Value (AOV): $542

- Impressions Delivered: 32.2 million views

- Following the initial pilot, Air Canada conducted a second campaign, achieving.

- 40% Incremental Lift among new customers

- 75% Incremental Lift among loyal customers

- New Customers: 7,475

- Incremental Sales: $2,270,172

- Total Sales: $5,166,599

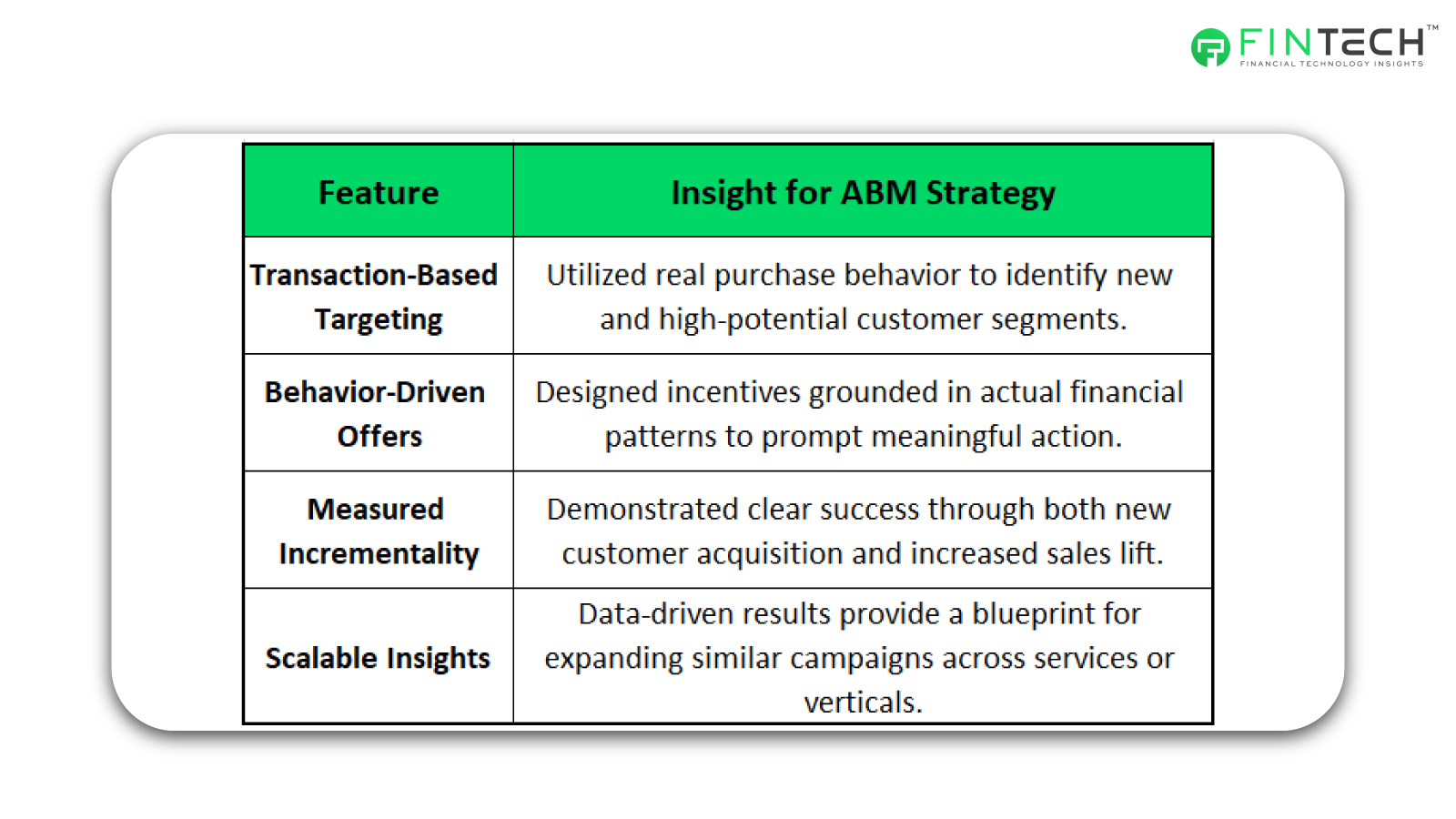

Why This Case Matters for ABM

This case demonstrates how payment data can be a driver of effective, measurable ABM marketing programs in the banking industry, when used safely and creatively.

Best Practices for Using Payment Data Responsibly in ABM

Payment data is an advantageous asset for banks administering account-based marketing programs.

However, it is sensitive data, and with that, there are regulatory and ethical accountability provisions closely tied to its access and exposure.

To account for every use, which balances marketing objectives with regulatory responsibility, can be a challenge and should come as no surprise. The following best practices will allow banks to consider both perspectives.

1. Respect Data Privacy Accountability

A bank (or any institution) operates in some of the most rigorous privacy regulations in the global financial services industry.

Many of those regulations are based on the same legal principle – that is, following the legal framework and provisions as dictated within the Gramm–Leach–Bliley Act (GLBA) in the US, the California Consumer Privacy Act (CCPA), or the European Union’s General Data Protection Regulation (GDPR) for international clients.

- Know the rules unique to your geographic area and customers.

- Design ABM strategies with restrictions consistent with those legal frameworks from the outset.

- Engage team members responsible for compliance when developing the campaign to ensure all legal obligations are in order.

2. Build Customer Trust

As with any banking relationship, trust is paramount. Customers expect the integrity, safety, and ethical use of their transaction data.

- Maintain transparency and share facts about how you will use their payment data to enrich their experience.

- Display privacy notices that are clear and understandable.

- Provide opt-outs that don’t require barriers to access core banking services.

3. Provide an Effective Data Governance Framework

An effective data governance structure can help ensure the integrity and safe use of payment data.

- Establish clear ownership for data quality and data accuracy.

- Descriptive processes for classifying, retaining, and deleting data.

- Monitor access to the data to prevent misuse.

4. Leverage Consent-Based Marketing

When using payment data in account-based marketing (ABM), the key factor is consent and consent management.

- Be explicit with your request to use transaction data for the stated purpose in your campaigns.

- Keep proper records of consent for each account.

- Provide requests for future consents following current campaigns or applicable regulations.

5. Align Marketing and Ethics

Compliance with legislation and regulations is one thing; advertising that lies within the bounds of ethics goes a bit further and asks whether it meets customers’ reasonable expectations or has some impact on society.

- Don’t run campaigns that may unduly coerce or prey on customer groups that may be vulnerable.

- Make sure that your campaign language and messaging align with the bank’s stated values and reputation.

- Go through a full review of the campaigns to be sure that the arms-length transactions are conducted fairly and transparently.

Overall responsible use of payment data in ABM is not only a compliance matter, but it can also be a business advantage. Banks sell trust in their relationship with customers, and that trust must include their use of their customers’ data in a responsible manner.

Banks that value privacy, respect the integrity of transaction data, and act honestly and transparently when communicating with customers improve their customer relationships and overall campaign outcomes.

By making these practices part of the daily operational routines of the organization, Financial Institutions can capitalize on data to grow while safeguarding the trust of their customers.

Conclusion

Banks that want to conduct effective account-based marketing now have an incredibly valuable strategic asset at their disposal – payment data.

This data ultimately delivers actionable intelligence based on actual, observed behavior. This means financial services organizations can understand which accounts to target with which messages when.

Any data-driven initiative must be mindful of privacy regulations, ethics, and consumer trust. The banks that succeed with account-based marketing tomorrow will be those that embrace the potential of payment data while remaining committed to ethical data use.

FAQs

1. What’s the future for payment data in ABM?

As AI and real-time analytics continue to evolve, payment data will be used to create even more hyper-personalized, compliance-driven campaigns.

2. What technologies assist banks in using payment data in ABM?

Banks typically use Customer Data Platforms (CDPs), advanced analytics solutions, and AI/ML marketing partners.

3. What is payment data in banking?

Payment data is the record of the transaction that was created whenever a consumer made a payment. This will typically include the amount, date, merchant, and payment method.

4. What can banks do to use payment data responsibly?

The bank should think about strong data governance, consent, anonymizing sensitive information, and audit trails.

5. How can banks use payment data in account-based marketing?

Banks can use payment data to understand payment behaviours and use that information to subsequently segment high-value accounts, personalize outreach, and identify cross-sell or upsell opportunities.

To participate in our interviews, please write to us at sudipto@intentamplify.com