The Evolution of Digital Transactions

Over the past decade, the landscape of digital transactions has significantly altered how we engage in commerce globally. This shift has provided consumers with enhanced speed, convenience, and transaction security. Among these aspects, safety remains a paramount concern within the payments ecosystem, particularly given the surge in digital commerce and the rise in data breach attempts and Man-in-the-Middle (MITM) attacks.

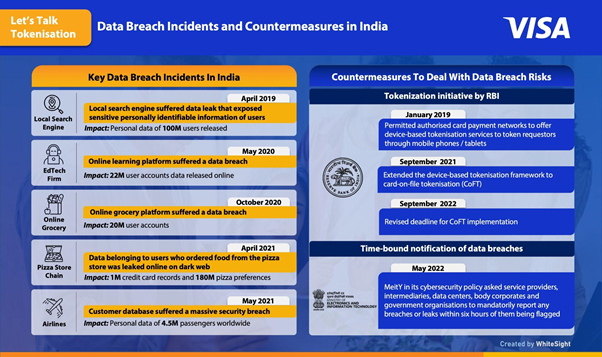

Since 2019, numerous banks and financial institutions have experienced data breaches that have impacted millions of users. In 2021, the frequency of cyberattacks and data breaches rose by over 15 percent compared to the previous year. These incidents represent only a fraction of the overall issue—beyond exposing customer data to malicious entities, they can severely damage a company’s reputation, which takes years to establish. Furthermore, projections suggest that by 2030, 74 percent of digital payments will occur through embedded platforms that integrate financial services into non-financial companies’ offerings, making the protection of consumer data more vital than ever.

Read: Identity Fraud: How Much Banks Lost in 2024?

Enhancing Security Through Tokenisation

Since the early 2000s, following the RBI’s approval of smart debit cards, there have been numerous regulations concerning card issuance and innovation. Security measures such as two-factor authentication (2FA), online alerts, compliance with PCI DSS standards, and the mandatory issuance of EMV chip cards have all been enacted over the last decade. The most recent advancement in this series of security innovations is tokenization. Tokenization has garnered significant attention from the RBI in recent years and is a globally recognized technology that enhances security while providing a smoother customer experience. Using tokenization, merchants are prevented from storing customer payment information; instead, they utilize a ‘token’ generated by the payment network for transactions. Since tokenization obscures the card number, sensitive information remains accessible only to issuers and card networks, with merchants only able to view the generated network token. This technology allows consumers to carry out recurring payments seamlessly without the concern of updating details when a card expires or is reissued, as the network token remains valid for a designated merchant or device once created.

- Card-on-File Merchant Transactions: Card-on-File Tokenisation (CoFT) where payment tokens are used in lieu of Card-on-File storage for e-commerce transactions

- Device-based Contactless Transactions: In-store contactless payments with device-centric digital wallets used through mobile phones and other devices (e.g., Google Pay, Samsung Pay, etc.)

- Device-based Remote Transactions: Tokens stored in payment apps in a mobile device and used for in-app e-commerce transactions

- Smart Devices Transactions: Payments made with wearables, tablets, or other Internet of Things (IoT) devices. (e.g., smart watches)

Read: Top 10 Trends Of Customer Experience: Why CX is the Cornerstone of FinTech Success?

The Rise of Embedded Finance

Today, a multitude of embedded financial products allows customers to access banking services on platforms owned by non-financial companies. These services are underpinned by automation and cloud payments, enhancing user experiences.

Diverse Payment Solutions

With tap-to-pay and scan-to-pay options like QR codes and virtual cards, consumers now enjoy a variety of flexible payment methods. Embedded card payments are crucial in propelling e-commerce strategies, creating a seamless buying journey for users.

Transforming Transit Payments

For frequent commuters and visitors alike, open-loop contactless transit solutions provide a quick and easy way to pay for rides. Companies like Visa are enhancing passenger experiences worldwide by offering secure digital solutions.

Payments in an Interconnected Future

As embedded payments continue to expand, we are moving toward an interconnected future. Experts believe that the technology driving this evolution will be led by the Internet of Things (IoT), with predictions suggesting that IoT-enabled devices will number around 75 billion by 2025. The explosive growth of IoT and IoT-led payments is likely as more connected devices and wearable technologies become payment-enabled.

The Role of Tokenisation

As tokenization becomes more widespread among acquiring and issuing banks and merchants, it will be fundamentally integrated into digital commerce. This integration is expected to unlock positive and smooth payment experiences for customers, merchants, and financial institutions while ensuring the integrity and safety of cardholder data across various entities.

Read: Fintech Marketing: Top 10 Power Strategies to Accelerate Growth

Read: Top 10 Strategies for Effective Fintech Branding

Thanks for reading!

To share your insights with the FinTech Newsroom, please write to us at news@intentamplify.com