What is a Central Bank Digital Currency (CBDC)?

A central bank digital currency (CBDC) is a type of digital currency that is issued by a country’s central bank. It is comparable to cryptocurrencies, with the exception that its value is established by the central bank and is equivalent to the country’s fiat currency. CBDCs are being developed by numerous countries, and some have even implemented them. It is crucial to comprehend the nature of CBDCs and their implications for society, as numerous nations are currently investigating methods to transition to digital currencies.

A central bank digital currency (CBDC) is the digital representation of a nation’s fiat currency. A CBDC is issued by a nation’s monetary authority, or central bank, to facilitate the implementation of monetary and fiscal policies and to promote financial inclusion. Numerous nations are investigating the potential impact of CBDCs on their financial networks, economies, and stability. It is crucial for individuals and nations to comprehend central bank digital currencies, as certain economies worldwide are transitioning to their utilization.

Read: Fintech in Hospitality: Top 10 Fintech Solutions for Hotels

Fiat money is a currency that is issued by the government and does not have any physical support, such as gold or silver. It is regarded as a legal tender that can be exchanged for products and services. In the past, fiat money was represented by banknotes and coins. However, technological advancements have enabled governments and financial institutions to augment physical fiat money with a credit-based currency model that digitally documents transactions and balances. Physical currency continues to be extensively accepted and exchanged. Nevertheless, its utilization has declined in certain developed nations, and this trend has been further exacerbated by the pandemic.Additionally, the introduction and development of blockchain technology and cryptocurrency have sparked a renewed interest in digital currencies and cashless societies. The utilization of government-backed digital currencies is currently being investigated by governments and central banks worldwide. In the same manner as fiat money, these currencies would be fully backed and supported by the issuing government when and if they are implemented.

Read: Top 10 Neobank Companies of the Fintech World

Uses of CBDCs

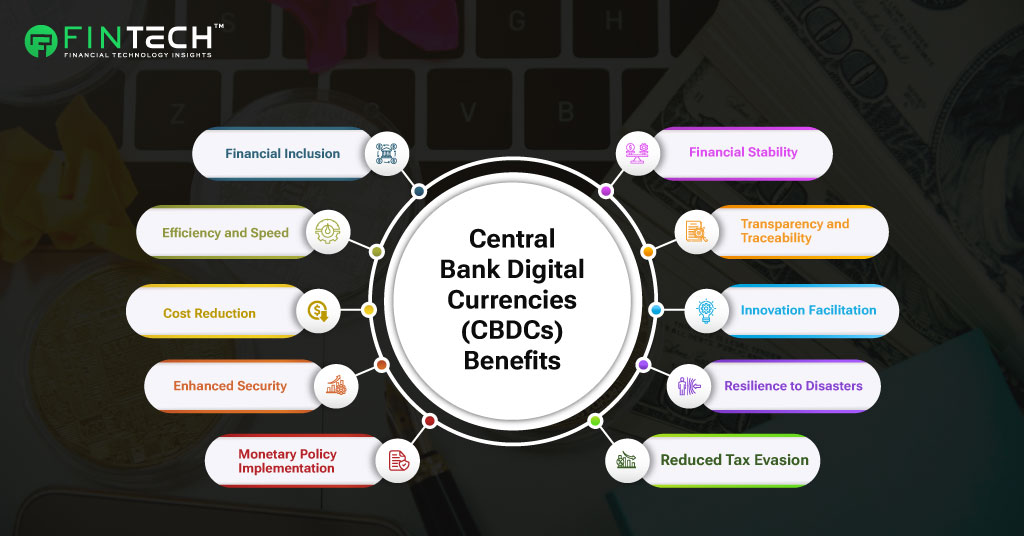

In the United States and numerous other countries, a significant number of individuals lack access to financial services. In 2023, 6% of adults in the United States were without a bank account.Two The figures are significantly higher in numerous other countries. Given this, the primary objectives of CBDCs are as follows: To offer financial security, convenience, transferability, privacy, and accessibility to businesses and consumers who conduct financial transactions. Reduce the cost of maintenance required by a complex financial system, reduce cross-border transaction costs, and offer lower-cost options to individuals who currently use alternative money-transfer methods.

Diminish the hazards associated with the utilization of digital currencies, or cryptocurrencies, in their present state. The value of cryptocurrencies is subject to significant fluctuations, rendering them highly volatile. This volatility has the potential to significantly impact the stability of an economy and result in severe financial duress for numerous households. Households, consumers, and businesses would have a secure method of exchanging digital currency through CBDCs, which are guaranteed by a government and regulated by a central bank. A central bank is also equipped with the ability to implement monetary policies in order to control growth, influence inflation, and ensure stability through the use of a CBDC.

Read :Top 5 Reasons Why Sysdig Is Used by Goldman Sachs

CBDCs of Different Types

CBDCs are classified into two categories: wholesale and retail. Wholesale CBDCs are primarily utilized by financial institutions, while retail CBDCs are utilized by consumers and businesses.Four

Wholesale CBDCs

Wholesale CBDCs operate similarly to central bank reserves. An institution is granted an account by the central bank to deposit funds or to resolve interbank transfers. Central banks may establish interest rates and regulate lending by employing monetary policy instruments, including reserve requirements or interest on reserve balances.

Retail CBDCs

Retail CBDCs are digital currencies that are backed by the government and are utilized by both consumers and enterprises. The risk of intermediary risk, which is the possibility that private digital currency issuers may go insolvent and lose customers’ assets, is eliminated by retail CBDCs.

- They differ in the manner in which individual users access and utilize their currency.

- Private keys, public keys, or both are required to access token-based retail CBDCs. Users can execute transactions anonymously using this validation procedure.

- Digital authentication is necessary to access an account in account-based retail CBDCs.

- The two varieties of CBDCs can be developed and implemented in a manner that ensures they operate within the same economy.

Issues Concerning CBDCs

The Federal Reserve has identified issues addressed by CBDCs, as well as matters that must be addressed before a CBDC can be designed and implemented.

Issues Addressed By CBDCs

- Free from credit and liquidity risk

- Lower cross-border payment costs

- Support the international role of the dollar

- Aim for financial inclusion

- Expand access to the general public

Issues Created by CBDCs

- Financial structure changes

- Financial system stability

- Monetary policy influence

- Privacy and protection

- Cybersecurity

Problems Addressed by CBDCs

- Reduce the risk of third-party events, such as bank failures or bank raids. The central bank is responsible for any residual risk that persists in the system.

- Increased jurisdictional cooperation between governments and the reduction of complex distribution systems can reduce high cross-border transaction costs.

- Could sustain and safeguard the dominance of the U.S. dollar, which remains the most widely used currency in the world.

- To provide financial access to the unbanked population, the cost of implementing a financial structure within a country is eliminated.

- Can eliminate the necessity for costly infrastructure by establishing a direct connection between consumers and central institutions.

Read: 10 AI ML Applications in the Identification and Prevention of Different Types of Fraud

Problems Caused by CBDCs

- The potential impact of a significant change in the financial structure of the United States on the economy, household expenses, investments, banking reserves, interest rates, and the financial services sector is currently undetermined.

- The stability of a financial system may be impacted by a transition to a CBDC, which is currently unknown. For instance, withdrawals may not be facilitated during a financial crisis due to insufficient central bank liquidity.

- Monetary policy is implemented by central banks to influence inflation, interest rates, lending, and spending, which in turn impacts employment rates. The economy must be positively influenced by central banks, which must possess the necessary instruments.

- One of the most significant factors driving cryptocurrency is privacy. The monitoring of financial offenses by authorities is crucial for CBDCs, as it supports efforts to combat money laundering and the financing of terrorism. Therefore, an appropriate level of intrusion is necessary.

- Hackers and criminals have targeted cryptocurrency. The same group of criminals would likely be attracted to a digital currency issued by a central bank. Consequently, it would be necessary to implement a robust strategy to prevent system penetration and the seizure of information and assets.

Cryptocurrencies in Comparison to CBDCs

- The cryptocurrency ecosystem offers a glimpse of an alternative currency system in which the terms of each transaction are not dictated by burdensome regulations. Consensus mechanisms that prevent tampering secure these transactions, which are difficult to duplicate or counterfeit.

- Central bank digital currencies are intended to resemble cryptocurrencies; however, they may not necessitate blockchain technology or consensus mechanisms.

- Furthermore, cryptocurrencies are decentralized and unregulated. Their value is determined by user interest, utilization, and investor sentiments. These assets are more suitable for speculation than for use in a financial system that necessitates stability, as they are volatile. CBDCs are intended to provide stability and security, and their value is comparable to that of fiat currency.

CBDCs in Development and Use

- In an effort to ascertain the feasibility and practicality of a central bank-controlled digital currency (CBDC) in their respective economies, numerous countries have implemented pilot programs and research projects.8

- The Bahamas, Jamaica, and Nigeria were the only three countries that had a functioning CBDC as of March 2024. For technical reasons, the Eastern Caribbean Currency Union suspended its CBDC and initiated a new pilot program.

- Eight of the G20 have programs in development, and there are 36 CBDC prototypes in operation. The BRICS countries—Brazil, Russia, India, China, and South Africa—are currently investigating the establishment of a CBDC.

- Britcoin, which operated from 2011 to 2019, is an illustration of an unsuccessful CBDC endeavor.Nine

- The Federal Reserve has indicated that the United States is among the countries that are investigating the potential of a central bank depository (CDB) to enhance the safety and efficiency of its domestic payments system.

Read: Top 5 Strategies for Cloud Security Regulations in Financial Services by Sysdig

What is the objective of a CBDC?

CBDCs are digital currencies that are supported by the government and utilize blockchain or distributed ledger technology. Their objective is to reduce the maintenance expenses of existing monetary systems and increase the accessibility of financial services.

Is the United States transitioning to digital currency?

Not yet. The Federal Reserve and its branches are currently conducting research on CBDCs and the potential methods of integrating them into the U.S. financial system. The development of a national strategy on digital currencies was mandated by President Joe Biden.

Is CBDC a threat?

CBDCs should be implemented to complement existing financial networks and fiat currencies, rather than to supplant them. One could potentially disrupt a system if it were implemented to replace a fiat currency; however, no nation has yet to implement it, rendering the potential consequences either hypothetical or unknown.

Conclusion

Several countries are currently engaged in the research or development of central bank digital currencies, and three have already implemented them. The primary objective of a CBDC is to offer financial security, convenience, transferability, privacy, and accessibility to both enterprises and consumers.

Read: Fintech Marketing: Top 10 Power Strategies to Accelerate Growth

Thanks for reading!

To share your insights with the FinTech Newsroom, please write to us at news@intentamplify.com