Personalized campaigns for banking tech buyers are no longer a marketing luxury.

Today’s financial technology market has evolved so that decision makers expect to be engaged meaningfully every time they interact.

They want to discover solutions that solve their business pain points, comply with their regulatory environment, and fit strategically into their growth plans.

It is often the case that the banking technology market is complex to successfully navigate, as the end customer at the decision point of a transaction is usually composed of multiple people, and long cycles of evaluation are the norm.

In this high-stakes environment, generic messages won’t work. Campaigns need to be specific and meaningful to the situation of the buyer, alongside being data-driven.

The advancement of artificial intelligence, predictive analytics, and various marketing automation tools has changed the personalization landscape in marketing. Now we can not only be predictive about needs, but we can also provide relevant content at every single touchpoint, from awareness to purchase.

We can do it every day, consistently. For marketers, it translates to more engagement and generally improved conversion rates. For the buyers, it means receiving relevant insights and offers delivered in a way that is aligned with their objectives.

In this article, we will outline how financial technology marketers can leverage these techniques to create personalized campaigns that resonate with banking tech buyers.

Understanding the Banking Tech Buyer

A banking tech buyer operates under a high level of regulatory scrutiny in one of the most risk-averse sectors on the planet.

Their purchasing decisions are strategic, usually high-value, and regularly long-term. Marketers must understand who the buyer is, where they are influenced, and how they make decisions about possible solutions to have much success with targeted personalized campaigns.

Banking tech buyers are not impressed by generic marketing messages. Their attention is drawn to a narrative or marketing message that isolates their operational challenges, compliance concerns, or business opportunities. Therefore, the only way for us to get their attention is to be a precise, authoritative, and industry-informed communicator.

Banking tech buyers have a variety of characteristics in common, not limited to the following:

The Roles Include:

- The CIOs, CTOs, Chief Digital Officers,

- Head of IT Infrastructure,

- Digital Transformation Leaders.

Decision-making approach:

- Multiple influencers,

- cross-functional and approvals,

- Risk assessments,

- Everything from potential data loss to their action plan if there is an environmental catastrophe.

Critical considerations:

- Security,

- Compliance,

- Scalability,

- ROI, and

- Vendor credibility.

Industry context:

Banks operate in a world of highly variable regulatory requirements, rapidly accelerating technologies, and constant competitive pressure from fintech disruptors.

Their top pain points usually relate to:

- Inflexibility and lack of innovation are typically associated with legacy systems.

- The rising costs of maintaining legacy infrastructure.

- Continuous pressure to deliver frictionless digital experiences to customers.

- Increased pressure to prevent cybersecurity and fraudulent behavior.

- Integrating with existing systems is tricky.

Understanding these factors is essential in building campaigns that resonate. These campaigns should be credible for banking tech buyers.

Mapping their buying journey while aligning your marketing touchpoints to their journey stages, fintech marketers will better connect with banking tech buyers and establish credibility and trust.

Why Personalization Is Important in Banking Technology Marketing

Banking technology buyers expect timely and relevant communications. Most buyers see generic outreach as noise and don’t pay attention. Evidence suggests that customers and clients are increasingly expecting personalized interactions and are well aware when firms fall short on personalization.

Furthermore, personalization moves business outcomes. Studies indicate that good personalization can often boost revenue in double digits. Personalization can be a lot more than a good-to-have.

Brian Moynihan, CEO, Bank of America, says:

Our emphasis on personalized financial solutions and superior customer service has strengthened customer loyalty, attracted new clients across all our businesses,”

The Key Points to Remember:

- Instills trust in a high-risk-averse sector. Banking buyers assess vendors on credibility and relevance. Personalization indicates you understand their constraints as well as priorities.

- According to Krungsri Research, Hyper-personalization can raise a bank’s revenue by up to 15%, while improving marketing ROI by up to 30%

- Increases intent to purchase. Third-party research indicates significant portions of customers are more inclined to buy when receiving personalized experiences, which stimulates pipeline conversion.

- Heightens retention and lifetime value. Organizations that place a high value on personalization have better retention rates and repeat purchase rates – an important value add for long B2B buying cycles.

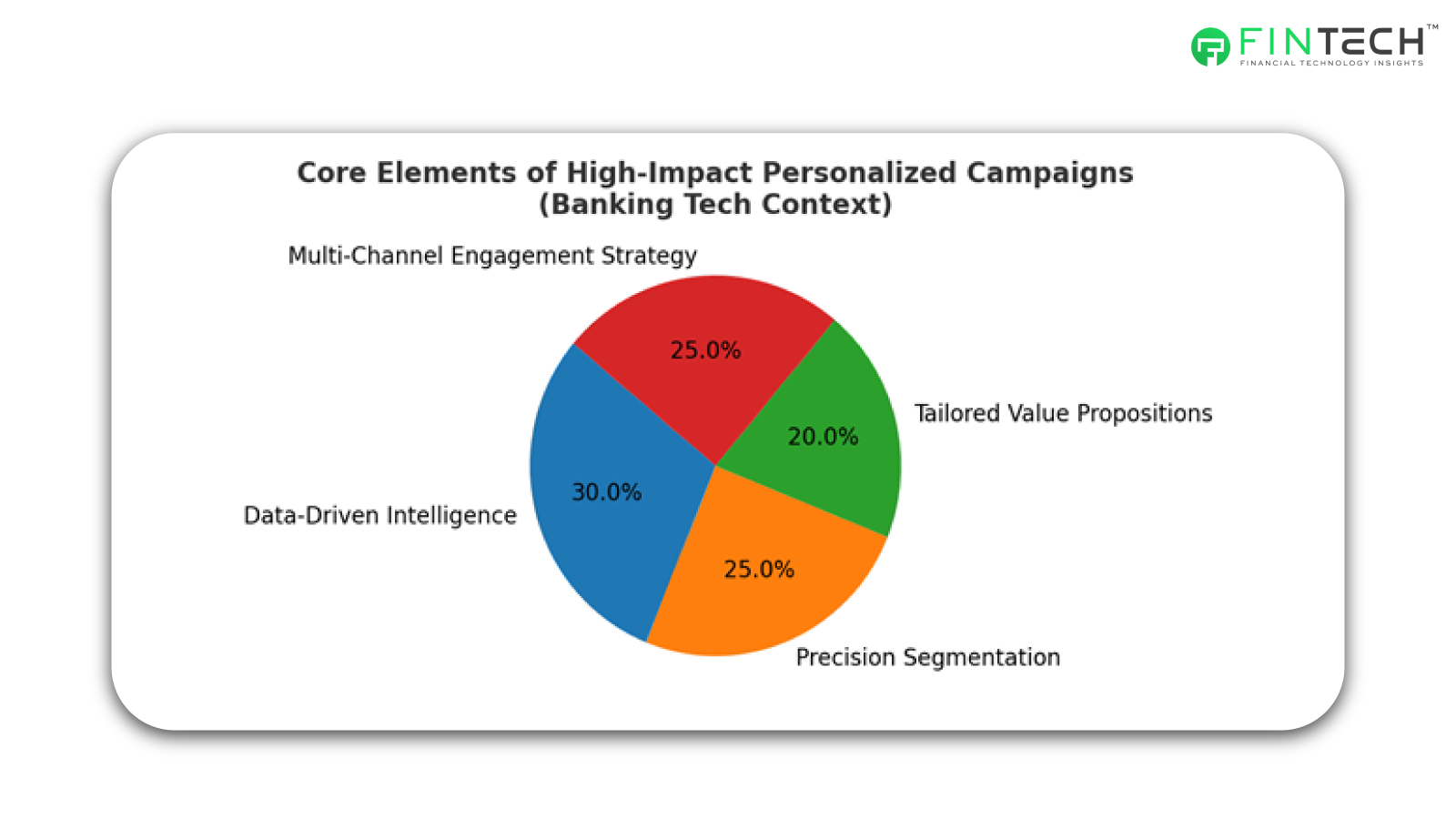

Core Components of High-Impact Personalized Campaigns

Personalized campaigns for banking technology buyers require a little more than the segmentation of data.

They require an approach that manages the complexity of financial technology decision-making, risk-adverse banking environments, and compliance regulations.

Successful campaigns bring to bear three components – accurate market intelligence, pinpointed audience segmentation, and multi-channel orchestration. These campaigns are designed to encompass the technology roadmap of the bank, the regulatory requirements of the bank, and digital transformation initiatives defined by the bank.

Key components include:

Data-Driven Intelligence

- Use analytics from core banking systems, transactional data, and digital engagement metrics to build out the buyer’s profile.

- Embed the use of KYC (Know Your Customer) and CDD (Customer Due Diligence) insights as permitted by privacy; banks take privacy and the handling of personal information seriously.

- Leverage predictive modeling of buyer needs based on operational pain points. Examples include an aging infrastructure or missing capabilities due to the lack of scalability of the existing technology.

Precision Segmentation

- Segment buyers by institution size (i.e., community vs. international), technology maturity, and geographic regulatory environment.

- Segmenting the market by investment priorities, such as cloud migration, API-based banking, or payment modernization, helps you formulate the right messaging.

- You should also consider the institution’s capital expenditure cycles and budgeting process to align messaging better.

Targeted Value Propositions

- Tell ROI stories centered on banking KPIs, like improvements in the cost-to-income ratio of your clients, and the degree of impact on their net interest margin.

- You should be using risk-adjusted performance measures to position technology posturing for analysis of gains.

- Also, clearly describe how you can translate to measurable value in terms of compliance, operational efficiency, and customer retention.

Multi-channel Engagement Strategy

- By using direct messaging campaigns on LinkedIn InMail, participation in banking industry forums, private investor briefings, and sector-specific engagements such as webinars with banking industry representatives.

- Using your holiday whitepapers, compliance checklists, and digital maturity assessments as the value added instead of brand recognition

- When using email automation, CRM touchpoints, and account-based marketing platforms, ensure all pieces maintain the same messaging and content alignment.

A personalized, high-touch campaign doesn’t treat banking technology buyers like different pieces of a box; it steps outside the box to the strategic level of their decision-making and risk management processes.

The impacts include both now and long-term with regards to what those executives deem appropriate disclosures in the interest of their own or the institution’s integrity in changing technology.

Here’s a pie chart showing the relative weight of each **core element** in high-impact personalized campaigns for banking tech buyers. The percentages are illustrative, based on typical strategic emphasis.

Personalization Tactics Matched with Banking Tech Buying Stages

In banking technology, personalized campaigns work best when they align directly with the buyer’s current level in the decision-making process.

In banking tech, unlike many other buying situations, a purchase is rarely a decision made by 1 individual. It normally goes through a multi-tier approved chain, inter-departmental reviews, and compliance reviews before a banking tech solution can be purchased.

Step 1 – Awareness

The awareness stage is about positioning your brand as a credible expert voice in the banking technology landscape.

Buyers at this stage are not currently looking for vendor-specific solutions. They are focused on working out the trends, regulatory changes, or technologies that are emerging to have an impact on their institution.

Personalization tactics that work well at this stage include:

- Delivering thought leadership content,

- housing association-wide issues like API

- enablement/open banking, real-time payments adoption, ISO 20022 migration.

Sharing geo-specific regulatory updates that mirror the buyer’s jurisdiction under US federal regulations, state banking regulations, Basel III, etc.

Stage 2: Consideration

The buyer is now in the consideration stage, where they have recognized their problem and are evaluating potential resolutions. At this point, we are now moving from a broad-based educational approach to goals tied to the appropriateness of a solution.

Some high-impact activities in the Consideration stage include:

- Providing product comparison guides that compare your solution to industry standards while connecting capabilities to measures used in core banking, such as cost-to-income ratio or loan turnaround time.

- Provide ROI calculators to demonstrate quantified benefits by the buyer’s asset size, transaction flow, or branch network size.

- Providing case studies with similar banking institutions that show compliance improvements, operational efficiency, or measured savings.

Ultimately, the goal is to make it obvious that your solution is purpose-built for their environment, mitigating perception of risk, and improving buyer confidence.

Stage 3: Decision

During the decision stage, the buyer has narrowed down the choice and just needs to eliminate the last piece of friction or needs one final piece of validation to move forward.

The buyer’s job is to eliminate friction after the positive decision to move forward. The seller’s job is to validate their earlier claims and try to line up the implementation timeline with the institution’s operational calendar.

Key personalization techniques at this stage could include:

- Executive briefing for C-suite and board members that is personalized to the institution’s strategic initiatives and compliance roadmap.

- Regulatory compliance validation documentation that shows how your solution meets and could prove data security, KYC/AML, and audit standards.

- Customized implementation plans that are personalized to show consideration for the fiscal year budget, availability of IT resources, and training expectations for staff.

At this stage, personalization is about risk mitigation- conveying that your company recognizes the high-stakes nature of banking technology procurement.

Stage 4: Post-Purchase & Retention

The post-purchase stage is often forgotten by marketers, and yet this is where the long-term value and advocacy are developed for banking technology vendors.

A satisfied client can be a repeat customer and vocal industry advocate.

Retention-focused personalization includes:

- Providing usage analytics that illustrate the achievement of ROI and operational efficiencies since activation.

- Introducing continual training paths for end users, IT Administrators, and compliance cohorts, and ensuing optimal product use.

- Encouraging co-branded success stories that reflect the bank’s innovation thought leadership while silently reinforcing the value of your solution.

This stage has transformed the vendor-customer relationship into a strategic partnership, which is significant in an industry where making the switch to a new vendor can be disruptive and expensive.

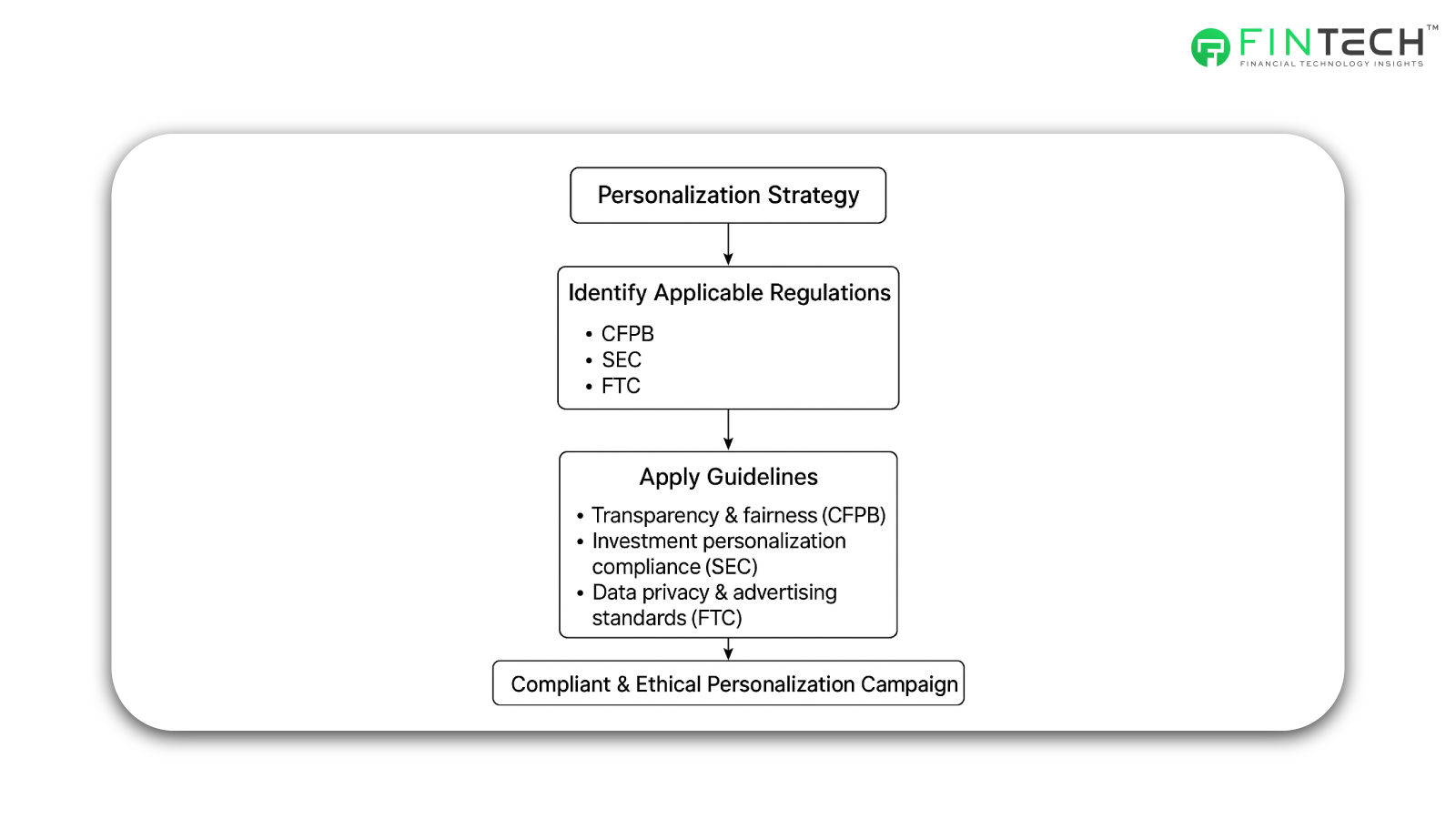

Compliance and Ethical Expectations

In banking, personalization strategies will inevitably be subject to significant regulatory scrutiny in the financial services industry.

Any financial institution that does not adhere to applicable legal and ethical expectations may subject itself to hefty fines, negative reputational effect, and/or loss of customer trust.

Compliance is not a simple checkbox compliance; compliance is part of responsible personalization, ensuring the marketing practice remains open, fair, and customer-centric.

Here are a few of the regulatory bodies and how they may impact personalized banking campaigns:

- Consumer Financial Protection Bureau (CFPB) – Oversees the vast consumer financial products and services, ensuring personalized offers and communications remain open, fair, and non-deceptive.

The CFPB guidelines help banks to avoid misleading practices while fulfilling customer data-driven offers.

- Securities and Exchange Commission (SEC) – Regulates personalization about investment, particularly for wealth management, portfolio recommendations, and targeted investment products.

An artificial intelligence recommendation for a fund must comply with SEC disclosure and suitability.

- Federal Trade Commission (FTC) – Regulates marketing practices to protect consumers from deceptive advertising and misuse of consumer data for personalized campaigns.

Most significantly, the FTC determines privacy expectations for banks about how they collect, store, and use consumer data.

Main ethical considerations for banks

While lawfulness is the bare minimum, ethical personalization in banking requires going beyond compliance to embed fairness, inclusivity, and trust:

- Data Transparency – Be completely explicit to customers as to how you collect, store, and use their data.

- Consent-Focused Personalization – Always obtain permission from customers before using their personal or behavioural data to target promotional offers.

- Algorithmic Bias – Audit AI and analytics platforms for inadvertent discriminatory or biasd against offer targeting.

- Security First – Always use strong encryption and fraud detection to protect sensitive financial data.

By embedding compliance and ethical responsibility into the entire personalization process, banks can enhance customer trust while providing personalized experiences in exchange for personal data, while remaining compliant.

Flowchart showing how personalization strategies align with CFPB, SEC, and FTC compliance checkpoints.

Conclusion

Fintech personalization is not just a competitive advantage anymore; it is an expectation. With personalization, though, comes a great burden and obligation to provide data privacy, transparency, and fairness.

Fintechs can mitigate the regulatory risks associated with personalization by linking personalization strategies to compliance frameworks from regulators like the CFPB, SEC, and FTC while still providing relevant and trustworthy experiences to consumers.

Finding the right balance between innovation and compliance not only protects consumers but also builds long-term brand trust in an increasingly regulated marketplace.

FAQs

1. Are there global compliance standards for fintech personalization?

All countries have different compliance-related organizations. Although the U.S. has the CFPB, SEC, and FTC, the European Union has GDPR, for example, which has severe implications for personalization.

2. What are the risks of non-compliance in fintech personalization?

Non-compliance poses risks of fines, lawsuits, reputational harm, loss of customers’ trust, and potentially a significant decrease in market share and growth.

3. What is the SEC’s role in personalization?

The SEC regulates personalization in investment-related products and services, such as portfolio recommendations and targeted investment products that meet investor protection criteria.

4. How does the FTC regulate fintech personalization?

The Federal Trade Commission (FTC), regulates advertising and marketing practices and prevents deceptive personalization and/or use of consumer data through targeted campaigns.

5. Why is compliance important in fintech personalization?

Compliance ensures that personalized offers, recommendations, and communications are transparent, fair, and respect consumer privacy. It protects both the company and its customers from legal and reputational risks.

To share your insights with the FinTech Newsroom, please write to us at sudipto@intentamplify.com