Data-driven sustainability in B2B fintech is reshaping the way financial technology firms approach growth and responsibility.

Sustainability has moved from the back seat to the front of the strategic bus in today’s business environment. It influences investment, compliance, and trust with clients. Companies, particularly in the B2B fintech space, are facing increased scrutiny and expectations to demonstrate measurable performance related to ESG (Environmental, Social, and Governance). Their conduct of business must follow the guidelines of regulators, corporate clients, and institutional investors.

The real challenge lies in being able to move beyond broad commitments to measurable performance.

This is where data becomes valuable. Fintechs can collect, analyze, and act upon reliable ESG data to measure their ESG performance and reduce the environmental and social impact of their operational activities. Also, they can track their potential for additional investments. Data helps firms improve efficiencies. It assists in identifying risks and potential areas of sustainable investment, and provides transparency to demonstrate compliance and build client relationships.

For B2B fintechs, moving to a data-driven approach for sustainability, ESG, and impact is more than a compliance exercise; it becomes a way of future-proofing their operations, positioning themselves as trusted partners, while generating a meaningful impact to enhance ongoing business growth.

What Is Data-Driven Sustainability in B2B FinTech?

Data-driven sustainability in B2B fintech is the use of technology, analytics, tools, and real-time information to track, measure, and improve environmental, social, and governance performance.

Rather than taking broad commitments to sustainability or relying on mental or manual reporting of sustainability practices, fintechs can now use data to provide evidence of measurable results.

Data-driven sustainability consists of five key elements.

Definition in Context

From a data-driven sustainability standpoint, fintech firms monitor ESG elements using digital tools, transaction data, and analytics. This includes carbon emissions, energy use, workforce practices, and governance issues.

New Process

Traditional reporting practices often involve manual data input, so there may be inaccuracies and delayed reporting if the reporting process is irregular.

A data-driven sustainability approach eliminates the inaccuracies and lagging information because real-time updates during an engaged transaction process are critical in the fast-moving financial service sector.

Integration into Business Strategy:

Data is a powerful compliance tool, but also for product innovations, partner selection, and managing risks.

This integration allows fintechs to balance the growth side of sustainability with their responsibilities.

Value for Stakeholders:

Clients, investors, and regulators want proof, not promises! Data provides the evidentiary basis to show you have real ESG performance and support for effectiveness and credibility.

Foundation for the Future

The tightening regulatory environment and increasing expectations allow fintechs to not only define sustainability through data but also better position themselves for competitiveness and trust.

The framework also allows B2B fintechs to move ESG from being just a complex responsibility or task into a measurable process that can be acted upon. The framework sets out a world where ESG is no longer treated as just an initiative. Instead, it is a business process that drives sustainable growth and resiliency..

Why Sustainability Matters in B2B FinTech

For B2B fintech firms, sustainability is the topmost priority. Regulatory Technology (RegTech) has enforced that data-driven sustainability is not compromised at any point in time.

Organizations that embed ESG into their strategy are in the best position to help reduce risks, develop trust, and unlock growth.

Key Points:

Regulatory Scrutiny:

Governments are imposing legislation implementing more stringent ESG reporting. Organizations are required to track and report their data on emissions, governance, and employee engagement, or else B2B fintechs will not be market-ready.

Client Expectations:

Corporate clients expect their partners to uphold the same values as their sustainability commitments. Providers that are open about their ESG data will be favoured when clients are procuring services and negotiating long-term contracts.

Investor Priorities:

Capital is being earmarked for fintechs that either have or are working on a credible ESG strategy. Organizations that construct a solid engagement with sustainability will have better access to funds and create comfort amongst investors.

Competitive Differentiation:

Firms embedding sustainability will gain a competitive advantage over their competition. Deploying responsible business practices will build reputation, attract clients, and alleviate pressure when securing industry partnerships.

Long-term value:

ESG engagement leads to reduced operational risks, increases efficiencies in business operations, and creates resilience amongst organizations. Consequently, this creates a platform for sustained growth in our evolving financial ecosystem.

B2B fintechs need to recognize that sustainability is not a compliance exercise. It is the core of modern decision-making, and inescapably linked to an organization’s performance, competitiveness, and future relevance as financial services evolve into 2050 and beyond.

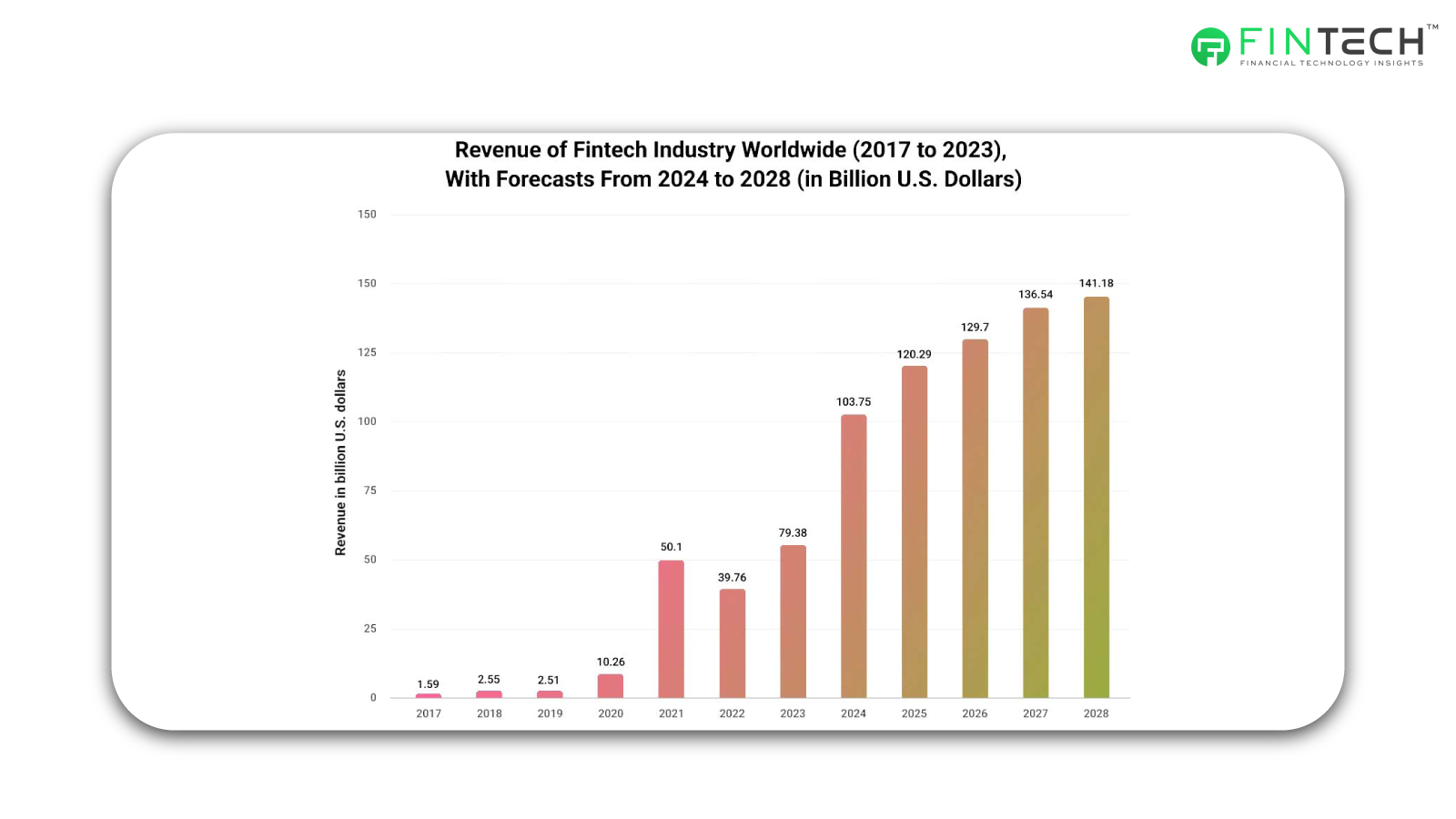

Fintech Growth and the Sustainability Imperative

- The chart indicates the incredible growth in revenue from the global fintech industry, increasing from $1.59 billion in 2017 to an estimated $141.18 billion by 2028.

- This growth explains why being sustainable must be very important. As the industry scales at this rate, its environmental and social impacts will also scale.

- The forecast also creates a path for a robust business case for data-led sustainability. With this level of growth, regulators, customers, and investors will demand increased consideration for ESG (environmental, social, and governance) accountability.

- The trend also shows that B2B fintech companies must take data-led measures to implement sustainability at scale because there is simply not enough time and resources in manual reporting to keep up with the expansion of the industry itself.

This level of growth demands both more opportunity and more responsibility. As revenues grow at this level, so too will the industry’s impact on the environment and society.

This takes sustainability from being a special project to a core business priority.

For B2B fintechs, being data-led in sustainability is the only way to keep pace with rising expectations, maintain trust, and responsibly scale in the upcoming years.

FinTech Sustainability Regulations in the U.S.

Unlike many international variables, there is no unique regulator of fintech sustainability in the United States. Instead, fintech sustainability laws are governed by the requirements and procedures of existing financial and consumer protection regulatory agencies:

-

Consumer Financial Protection Bureau (CFPB)

CFPB is a financial regulator that protects consumer rights and promotes fair practices for the fintech services it oversees.

-

Securities and Exchange Commission (SEC)

SEC requires publicly traded companies to disclose material climate risks and the risks of environmental, social, and governance (ESG) issues it is facing, or could face, affecting the transparency of their investors.

-

Federal Deposit Insurance Corporation (FDIC)& Office of the Comptroller of the Currency (OCC)

FDIC and OCC supervise the overall financial system, as well as consider climate-related risk and other ESG factors in their supervision processes.

-

Federal Trade Commission (FTC)

FTC is the prime enforcer for prohibiting deceptive practices such as “greenwashing,” where a poor sustainability story is deceptively crafted to make it look better.

Within this array of laws and regulators, fintech firms have access to a jumble of regulatory mechanisms that create indirect laws affecting how they report on sustainability and recognize sustainability in their actions.

Conclusion

Sustainability that is data-driven is now a strategic necessity for B2B fintechs rather than an option. As the busy sector continues to grow rapidly, any firm that utilizes ESG data will be in a better position to meet regulations, build client trust, attract investor confidence, and scale responsibly.

Sustainability practices in fintech are transitioning from being a side function to becoming a vital part of the core business activity. By integrating measurable ESG practices into their operations, fintech firms can turn compliance into a competitive advantage and responsibility into an opportunity for creating long-term value.

The message is clear – within the changing financial ecosystem, the firms that will ultimately prevail will be those that can prove, rather than just promise, that they are committed to sustainable growth.

FAQs

1. What does the future of sustainability look like in B2B fintech?

Sustainability will transition from being a compliance necessity to a driver of business growth. Fintech innovators that embed ESG into their strategy and leverage data will develop resiliency and ensure the sustainability of their business in the financial ecosystem.

2. What are the challenges that fintechs face in becoming more sustainable?

The challenges include decentralized regulation, complexity in gathering data, high costs of technology adoption, and ensuring accurate reporting and measurement of ESG performance.

3. Who are the U.S. regulators that regulate sustainability within fintech?

There is no single regulator, but agencies including the SEC, CFPB, FDIC, OCC, and FTC all oversee components of ESG disclosures, fair lending practices, climate risks, intersectionality with consumer protection, and greenwashing.

4. Why does sustainability matter in B2B fintech?

Sustainability demonstrates accountability to consumers and investors, protects against future regulatory repercussions, differentiates itself in the market competitive advantage while reducing cost and risk in the future.

5. How does ESG reporting impact fintech companies?

ESG reporting creates accountability to regulators, investors, and consumers. Fintech companies that demonstrate the ability to report on quantitative ESG risks and performance are more likely to receive contracts, investments, and regulatory approval.

To participate in our interviews, please write to us at sudipto@intentamplify.com